What Is Considered Excellent Credit? At WHAT.EDU.VN, we understand that navigating the world of credit scores can feel overwhelming. We’re here to break down what constitutes an excellent credit rating, how it benefits you, and the steps you can take to achieve it. Having a superior credit rating can unlock better financial opportunities. We will explore credit score ranges, the impact of credit utilization, and credit report analysis.

1. Understanding Credit Score Ranges

Credit scores are numerical representations of your creditworthiness, typically ranging from 300 to 850. These scores help lenders assess the risk of lending money to you. Different scoring models, like FICO and VantageScore, have slightly different ranges and criteria, but they generally align on what constitutes a good or excellent credit score.

1.1 FICO Score Ranges

The FICO score is one of the most widely used credit scoring models. Here’s a breakdown of the FICO score ranges and what they mean:

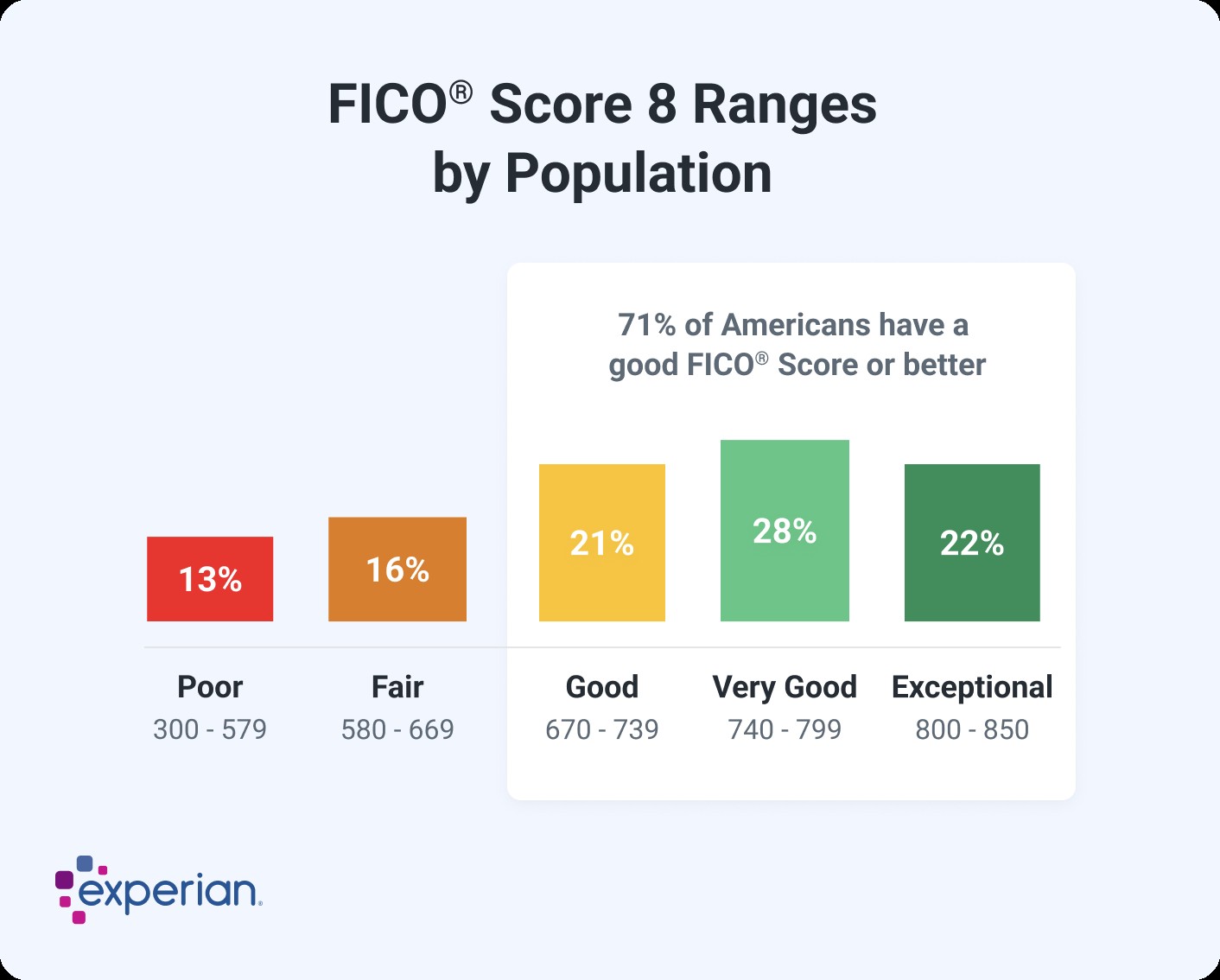

- Exceptional (800-850): This is the highest credit score range, indicating an extremely low credit risk.

- Very Good (740-799): A very good score suggests that you are a reliable borrower.

- Good (670-739): A good score indicates that you are a generally trustworthy borrower.

- Fair (580-669): A fair score may make it harder to get approved for loans or credit cards with favorable terms.

- Poor (300-579): A poor score suggests a high credit risk and can result in loan denials or high-interest rates.

1.2 VantageScore Ranges

VantageScore is another popular credit scoring model. Here’s how its ranges break down:

- Excellent (781-850): This is the highest range, indicating minimal credit risk.

- Good (661-780): A good score suggests you are a reliable borrower.

- Fair (601-660): A fair score may present challenges in securing loans or credit cards with favorable terms.

- Poor (300-600): A poor score indicates a high credit risk, potentially leading to loan denials or high-interest rates.

2. What is Considered Excellent Credit?

An “excellent” credit score generally falls within the highest tier of both the FICO and VantageScore models. Specifically:

- FICO: 800-850

- VantageScore: 781-850

Having a credit score in these ranges signals to lenders that you are an exceptionally reliable borrower. This can lead to significant financial benefits, which we’ll explore in the next section.

3. Benefits of Having Excellent Credit

Achieving an excellent credit score opens doors to numerous financial advantages. Lenders view you as a low-risk borrower, making you eligible for the best interest rates and terms on loans and credit cards. Here are some key benefits:

3.1 Lower Interest Rates

One of the most significant advantages of having excellent credit is access to lower interest rates. Whether you’re applying for a mortgage, auto loan, or credit card, a high credit score can save you thousands of dollars over the life of the loan. Lenders offer their best rates to borrowers with excellent credit because they are seen as less likely to default.

3.2 Better Loan Terms

In addition to lower interest rates, excellent credit can help you secure more favorable loan terms. This might include:

- Longer repayment periods: Giving you more time to pay off the loan with smaller monthly payments.

- Higher loan amounts: Allowing you to borrow more money for significant purchases like a home or car.

- Lower fees: Reducing or waiving certain fees associated with the loan.

3.3 Higher Credit Card Approval Odds

With excellent credit, you’re more likely to be approved for the best credit cards on the market. These cards often come with valuable rewards programs, such as cashback, travel points, and other perks. Additionally, you may qualify for cards with higher credit limits, providing you with more purchasing power and flexibility.

3.4 Improved Insurance Rates

In many states, insurance companies use credit-based insurance scores to help determine your premiums for auto, home, and life insurance. A good credit score can translate to lower insurance rates, saving you money on your monthly premiums.

3.5 Easier Rental Approvals

Landlords often check credit scores as part of the rental application process. Having excellent credit can make it easier to get approved for an apartment, especially in competitive rental markets. Landlords view high credit scores as an indicator of responsible financial behavior, increasing your chances of securing your desired rental property.

3.6 Negotiation Power

With excellent credit, you have more leverage to negotiate better deals with lenders and service providers. Whether you’re refinancing a loan or signing up for a new service, your strong credit profile gives you the upper hand in securing favorable terms.

4. Factors That Influence Your Credit Score

Several factors contribute to your credit score. Understanding these factors is crucial for maintaining and improving your credit health. Here are the primary elements that influence your credit score:

4.1 Payment History

Your payment history is the most critical factor in determining your credit score. It reflects your ability to make timely payments on your debts. Late payments, missed payments, and defaults can significantly lower your credit score. Conversely, consistently making on-time payments can boost your score over time.

4.2 Credit Utilization

Credit utilization refers to the amount of credit you’re using compared to your total available credit. It’s calculated by dividing your outstanding credit balances by your total credit limits. Experts generally recommend keeping your credit utilization below 30% to maintain a good credit score. High credit utilization can indicate that you’re overextended and may struggle to repay your debts.

4.3 Length of Credit History

The length of your credit history also plays a role in your credit score. Lenders like to see a long track record of responsible credit use. The longer you’ve had credit accounts open and in good standing, the better it is for your credit score.

4.4 Credit Mix

Having a mix of different types of credit accounts, such as credit cards, installment loans (e.g., auto loans, mortgages), and lines of credit, can positively impact your credit score. A diverse credit mix demonstrates that you can manage various types of debt responsibly.

4.5 New Credit

Opening too many new credit accounts in a short period can lower your credit score. Each time you apply for credit, it results in a hard inquiry on your credit report, which can slightly decrease your score. Additionally, lenders may view multiple new accounts as a sign of increased risk.

5. Steps to Achieve and Maintain Excellent Credit

Improving your credit score takes time and effort, but it’s well worth it in the long run. Here are some actionable steps you can take to achieve and maintain excellent credit:

5.1 Pay Bills on Time

The most important step is to consistently pay your bills on time, every time. Set up automatic payments or reminders to ensure you never miss a due date. Even a single late payment can negatively impact your credit score.

5.2 Keep Credit Utilization Low

Aim to keep your credit utilization below 30% on all your credit cards. If possible, pay off your balances in full each month. If you can’t pay in full, make sure to pay at least the minimum amount due to avoid late fees and negative marks on your credit report.

5.3 Monitor Your Credit Reports

Regularly check your credit reports from all three major credit bureaus (Experian, TransUnion, and Equifax) to ensure there are no errors or fraudulent activity. You can obtain free copies of your credit reports annually from AnnualCreditReport.com.

5.4 Avoid Opening Too Many New Accounts

Be mindful of how many new credit accounts you open, especially within a short period. Each application can result in a hard inquiry on your credit report, potentially lowering your score. Only apply for credit when you genuinely need it.

5.5 Maintain a Mix of Credit Accounts

If possible, maintain a mix of different types of credit accounts, such as credit cards and installment loans. However, don’t take on debt you don’t need just to improve your credit mix. Focus on managing your existing accounts responsibly.

5.6 Become an Authorized User

If you have limited credit history, consider becoming an authorized user on a credit card account held by a family member or friend with good credit. This can help you build credit history and improve your credit score over time.

5.7 Dispute Errors on Your Credit Report

If you find any errors on your credit report, dispute them with the credit bureau immediately. Provide documentation to support your claim and follow up to ensure the errors are corrected.

6. Common Misconceptions About Credit Scores

There are several common misconceptions about credit scores that can lead to confusion and poor financial decisions. Here are some myths debunked:

6.1 Checking Your Credit Score Hurts It

This is a common myth. Checking your own credit score does not hurt it. When you check your own credit, it’s considered a “soft inquiry,” which does not affect your score. Only “hard inquiries,” which occur when you apply for credit, can potentially lower your score.

6.2 Closing Credit Cards Improves Your Score

Closing credit cards can actually lower your credit score, especially if it increases your credit utilization ratio. When you close a credit card, you reduce your total available credit, which can negatively impact your credit utilization.

6.3 Carrying a Balance Improves Your Score

Carrying a balance on your credit card does not improve your credit score. In fact, it can hurt your score if it leads to high credit utilization. The best practice is to pay off your balance in full each month to avoid interest charges and maintain a low credit utilization ratio.

6.4 Credit Scores Are Only for Loans and Credit Cards

While credit scores are primarily used for loans and credit cards, they can also impact other areas of your life, such as insurance rates, rental applications, and even employment opportunities.

6.5 Everyone Has the Same Credit Score

Your credit score is unique to you and is based on your individual credit history. It can vary depending on the credit bureau and the scoring model used.

7. Understanding Credit Reports

Your credit report is a detailed record of your credit history. It contains information about your credit accounts, payment history, and any public records related to your credit, such as bankruptcies or judgments. Reviewing your credit report regularly is essential for identifying errors and monitoring your credit health.

7.1 What’s Included in a Credit Report?

A credit report typically includes the following information:

- Personal Information: Your name, address, Social Security number, and date of birth.

- Credit Accounts: Information about your credit cards, loans, and other lines of credit, including account balances, credit limits, payment history, and account status.

- Public Records: Information about bankruptcies, judgments, tax liens, and other public records related to your credit.

- Inquiries: A list of companies that have accessed your credit report, including both hard and soft inquiries.

7.2 How to Obtain Your Credit Report

You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) once every 12 months. You can request your free credit reports from AnnualCreditReport.com.

7.3 How to Read and Interpret Your Credit Report

Reviewing your credit report can seem daunting, but it’s essential for understanding your credit history and identifying any potential issues. Here are some tips for reading and interpreting your credit report:

- Verify Your Personal Information: Make sure your name, address, Social Security number, and other personal information are accurate and up to date.

- Review Your Credit Accounts: Check the status of each of your credit accounts and ensure that the balances, credit limits, and payment history are correct.

- Look for Errors: Carefully review your credit report for any errors, such as accounts you don’t recognize, incorrect balances, or late payments that you made on time.

- Check for Fraudulent Activity: Be on the lookout for any signs of fraudulent activity, such as unauthorized accounts or inquiries.

7.4 How to Dispute Errors on Your Credit Report

If you find any errors on your credit report, it’s crucial to dispute them with the credit bureau immediately. Here’s how to dispute errors:

- Gather Documentation: Collect any documentation that supports your claim, such as payment records, account statements, or other evidence.

- Write a Dispute Letter: Write a letter to the credit bureau explaining the error and providing copies of your documentation.

- Send Your Dispute: Send your dispute letter and documentation to the credit bureau by certified mail with return receipt requested.

- Follow Up: Follow up with the credit bureau to ensure that your dispute is being investigated and that the errors are corrected.

8. Credit Scores and Financial Goals

Your credit score plays a significant role in achieving your financial goals. Whether you’re planning to buy a home, purchase a car, start a business, or simply improve your financial well-being, having a good credit score can make it easier to reach your objectives.

8.1 Buying a Home

A good credit score is essential for getting approved for a mortgage with favorable terms. Lenders use your credit score to assess your creditworthiness and determine the interest rate and loan terms you’re eligible for.

To increase your odds of approval and qualify for a lower-rate mortgage, you should aim to have a credit score in the good range or higher. That’s a FICO® Score of at least 670.

The minimum credit score you need to buy a house could range from around 500 to 700, but will ultimately depend on the type of mortgage loan you’re applying for and your lender. Many lenders require a minimum credit score of 620 for a conventional mortgage. Other types of mortgages have different credit score requirements.

Remember that your credit score plays an important role in determining the interest rate and payment terms on a mortgage loan. Lenders base the interest they charge on how risky they view you as a borrower. So while it may be possible to get a mortgage with bad credit, you’re typically better off improving your score before you apply for a mortgage.

8.2 Buying a Car

Similar to mortgages, auto lenders use your credit score to determine your eligibility for an auto loan and the interest rate you’ll pay. A good credit score can help you secure a lower interest rate, saving you money over the life of the loan.

While there isn’t a set minimum credit score to buy a car, a VantageScore credit score of 661 or higher could be a good score. You’ll generally qualify for better auto loan terms as your score increases.

Auto lenders view low credit scores as a sign of risk, so an applicant with poor or fair credit will pay more in interest and might receive a lower loan limit. If you don’t have a good score, try to improve your credit before you buy a car.

8.3 Starting a Business

If you’re planning to start a business, your credit score can impact your ability to secure funding. Lenders and investors often review your credit history to assess your creditworthiness and determine whether to provide you with a loan or investment.

8.4 Renting an Apartment

Landlords often check credit scores as part of the rental application process. Having a good credit score can make it easier to get approved for an apartment, especially in competitive rental markets.

9. Building Credit From Scratch

If you have no credit history, it can be challenging to get approved for credit. However, there are several steps you can take to build credit from scratch:

9.1 Secured Credit Cards

A secured credit card is a type of credit card that requires you to provide a security deposit, which serves as collateral for the card. Secured credit cards are a good option for people with no credit history because they are easier to get approved for.

9.2 Credit-Builder Loans

A credit-builder loan is a small loan designed to help you build credit. The loan proceeds are typically held in a savings account, and you make monthly payments over a set period. Once you’ve repaid the loan, the funds are released to you.

9.3 Become an Authorized User

As mentioned earlier, becoming an authorized user on a credit card account held by a family member or friend with good credit can help you build credit history.

9.4 Report Rent and Utility Payments

Some credit reporting agencies allow you to report your rent and utility payments to help build credit. This can be a good option if you don’t have a lot of credit history.

10. Seeking Professional Advice

If you’re struggling to improve your credit score or have complex credit issues, consider seeking professional advice from a credit counselor or financial advisor.

10.1 Credit Counseling

A credit counselor can help you review your credit report, develop a budget, and create a plan for repaying your debts. They can also negotiate with your creditors to lower your interest rates or payment amounts.

10.2 Financial Advisor

A financial advisor can help you develop a comprehensive financial plan that includes strategies for improving your credit score, managing your debts, and achieving your financial goals.

11. Staying Informed and Proactive

Staying informed about credit scores and proactively managing your credit health is essential for maintaining excellent credit. Regularly review your credit reports, monitor your credit scores, and take steps to address any issues or errors you find.

11.1 Monitor Your Credit Scores

There are several ways to monitor your credit scores for free. Many credit card companies and banks offer free credit score monitoring services to their customers. You can also use free online tools like Credit Karma or Credit Sesame to track your credit scores.

11.2 Set Up Alerts

Set up alerts to notify you of any changes to your credit report or score. This can help you quickly identify and address any potential issues, such as fraudulent activity or errors.

11.3 Stay Educated

Stay educated about credit scores and credit management. Read articles, attend workshops, and follow reputable sources of financial information to stay up-to-date on the latest trends and best practices.

12. Credit Score FAQs

12.1 What is a good credit score range?

A good FICO score ranges from 670 to 739, while a good VantageScore ranges from 661 to 780. Scores above these ranges are considered very good or excellent.

12.2 How often should I check my credit score?

You should check your credit score regularly, at least once a month, to monitor your credit health and identify any potential issues.

12.3 How long does it take to improve my credit score?

The time it takes to improve your credit score depends on your individual circumstances and the steps you take to address any issues. However, with consistent effort and responsible credit management, you can see significant improvements in your credit score over time.

12.4 What is credit utilization?

Credit utilization is the amount of credit you’re using compared to your total available credit. It’s calculated by dividing your outstanding credit balances by your total credit limits. Experts generally recommend keeping your credit utilization below 30% to maintain a good credit score.

12.5 What is a hard inquiry?

A hard inquiry occurs when you apply for credit and a lender checks your credit report. Hard inquiries can slightly lower your credit score, but the impact is usually minimal and temporary.

12.6 What is a soft inquiry?

A soft inquiry occurs when you check your own credit report or when a lender checks your credit report for pre-approval offers. Soft inquiries do not affect your credit score.

12.7 How can I dispute errors on my credit report?

If you find any errors on your credit report, you can dispute them with the credit bureau by writing a letter explaining the error and providing supporting documentation.

12.8 Can I remove negative information from my credit report?

Negative information, such as late payments or defaults, can remain on your credit report for up to seven years. However, you can dispute any inaccurate or outdated information with the credit bureau.

12.9 What is a credit-builder loan?

A credit-builder loan is a small loan designed to help you build credit. The loan proceeds are typically held in a savings account, and you make monthly payments over a set period.

12.10 What is a secured credit card?

A secured credit card is a type of credit card that requires you to provide a security deposit, which serves as collateral for the card. Secured credit cards are a good option for people with no credit history.

13. The Future of Credit Scoring

The world of credit scoring is constantly evolving, with new models and technologies emerging all the time. Some of the trends shaping the future of credit scoring include:

13.1 Alternative Data

Credit scoring models are increasingly incorporating alternative data, such as rent payments, utility bills, and bank account information, to provide a more comprehensive view of a borrower’s creditworthiness.

13.2 Artificial Intelligence

Artificial intelligence (AI) and machine learning are being used to develop more sophisticated credit scoring models that can better predict a borrower’s likelihood of default.

13.3 Real-Time Data

Real-time data is being used to provide lenders with up-to-date information about a borrower’s creditworthiness, allowing them to make faster and more informed lending decisions.

13.4 Mobile Credit Scoring

Mobile credit scoring is emerging as a way to assess the creditworthiness of people in developing countries who may not have a traditional credit history.

14. Key Takeaways

- Excellent credit is generally defined as a FICO score between 800-850 or a VantageScore between 781-850.

- Having excellent credit can unlock better interest rates, loan terms, and credit card approvals.

- Key factors influencing your credit score include payment history, credit utilization, length of credit history, credit mix, and new credit.

- You can achieve and maintain excellent credit by paying bills on time, keeping credit utilization low, monitoring your credit reports, and avoiding opening too many new accounts.

- Building credit from scratch involves secured credit cards, credit-builder loans, and becoming an authorized user.

- Seeking professional advice from a credit counselor or financial advisor can be beneficial if you’re struggling to improve your credit score.

- Staying informed and proactive about your credit health is essential for maintaining excellent credit.

Achieving excellent credit is a worthwhile goal that can provide you with numerous financial benefits and opportunities. By understanding the factors that influence your credit score and taking proactive steps to manage your credit responsibly, you can improve your credit health and achieve your financial goals.

Have more questions about what is considered excellent credit? Don’t hesitate to ask the experts at WHAT.EDU.VN. We’re here to provide fast, free answers to all your questions. Visit our website at what.edu.vn or contact us at 888 Question City Plaza, Seattle, WA 98101, United States, or via WhatsApp at +1 (206) 555-7890. Let us help you navigate the world of credit and achieve your financial dreams.