What Is A Decent Credit Score? It’s a question many ask, and at WHAT.EDU.VN, we provide answers! A good credit rating is essential for financial well-being, unlocking better interest rates and loan terms. Discover what constitutes a good credit score, the influencing factors, and how to improve your creditworthiness. Let’s explore credit history, creditworthiness, and financial stability.

1. Understanding Credit Scores: The Basics

Credit scores are numerical representations of your creditworthiness, reflecting your ability to repay debts. They range from 300 to 850, with higher scores indicating lower risk to lenders. These scores play a crucial role in various financial decisions, from securing loans to renting apartments.

1.1. FICO Score vs. VantageScore

The two primary credit scoring models are FICO (Fair Isaac Corporation) and VantageScore. While both aim to assess credit risk, they differ slightly in their methodologies and the data they consider.

- FICO Score: The most widely used model, FICO scores are favored by lenders for their accuracy and reliability.

- VantageScore: Developed by the three major credit bureaus (Experian, TransUnion, and Equifax), VantageScore offers a competing model with its own scoring criteria.

1.2. Why Credit Scores Matter

A decent credit score is your financial passport, opening doors to various opportunities:

- Loans and Credit Cards: Qualify for loans and credit cards with favorable interest rates and terms.

- Mortgages: Secure a mortgage with lower interest rates, saving you thousands over the life of the loan.

- Rentals: Increase your chances of approval for apartments and rental properties.

- Insurance: Obtain lower insurance premiums on auto, home, and life insurance.

- Employment: Some employers may review your credit report as part of the hiring process.

2. What is Considered a Decent Credit Score?

Defining a decent credit score depends on the scoring model used. Here’s a breakdown of the ranges for both FICO and VantageScore:

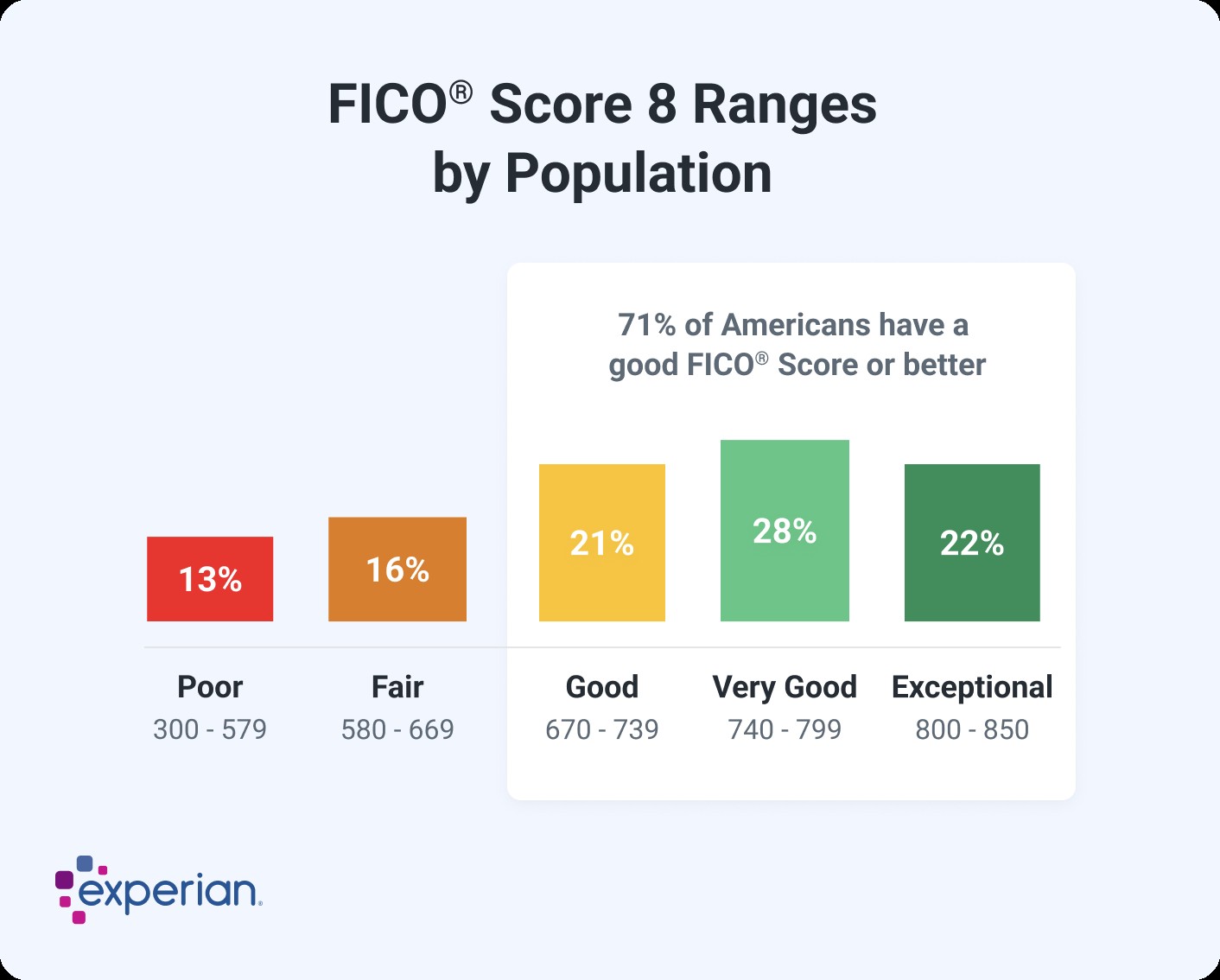

2.1. FICO Score Ranges

- Excellent (800-850): Top-tier creditworthiness, qualifying for the best interest rates and terms.

- Very Good (740-799): Above-average creditworthiness, with excellent approval odds.

- Good (670-739): Considered a decent score, opening doors to many financial products.

- Fair (580-669): Subpar creditworthiness, potentially facing higher interest rates and limited options.

- Poor (300-579): High-risk creditworthiness, with difficulty obtaining credit.

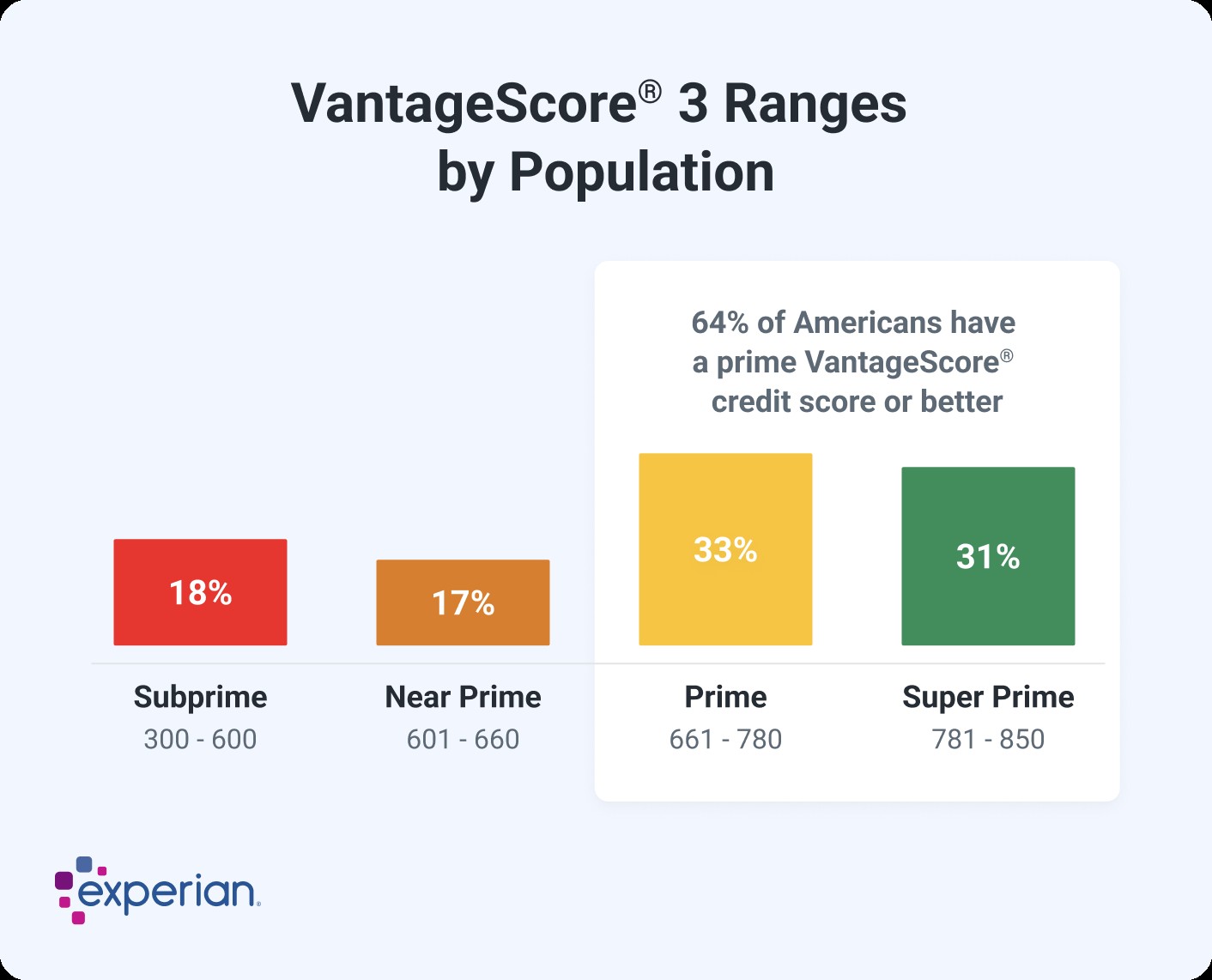

2.2. VantageScore Ranges

- Excellent (781-850): Top-tier creditworthiness, similar to FICO’s excellent range.

- Good (661-780): Considered a decent score, aligning with FICO’s good range.

- Fair (601-660): Subpar creditworthiness, similar to FICO’s fair range.

- Poor (300-600): High-risk creditworthiness, comparable to FICO’s poor range.

2.3. What a “Decent” Score Means in Practice

A score in the “good” range, whether FICO or VantageScore, generally means you’re a responsible borrower. Lenders view you as less risky, increasing your chances of approval and offering more favorable terms.

3. Factors Influencing Your Credit Score

Several factors contribute to your credit score. Understanding these factors is key to maintaining or improving your creditworthiness.

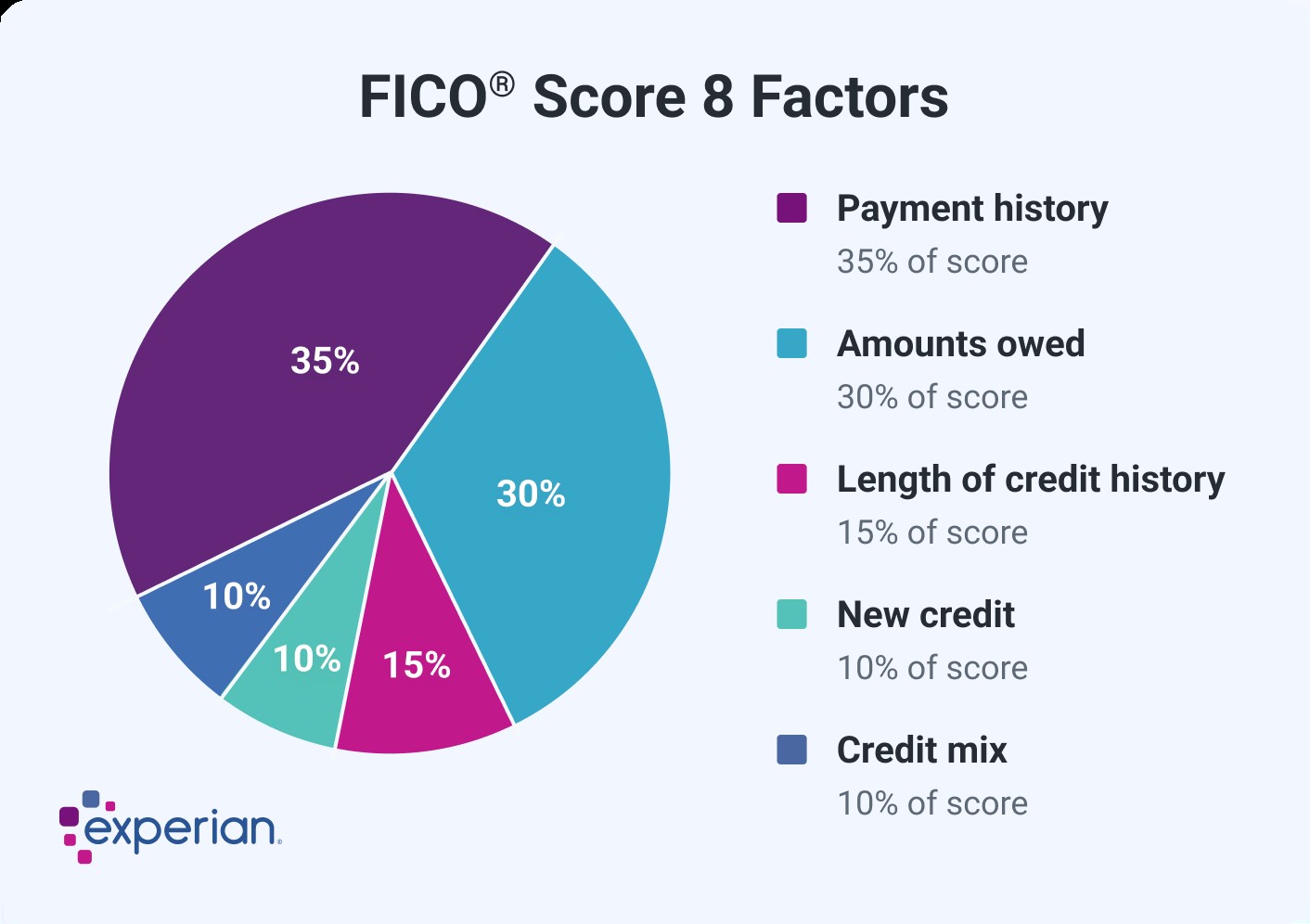

3.1. Payment History

- Importance: The most significant factor, accounting for 35% of your FICO score.

- Impact: Making on-time payments consistently demonstrates responsible credit behavior.

- Tips: Set up automatic payments to avoid missed deadlines.

3.2. Amounts Owed

- Importance: The second most influential factor, contributing 30% to your FICO score.

- Impact: High credit utilization (the amount of credit you’re using compared to your total available credit) can negatively impact your score.

- Tips: Keep your credit utilization below 30% for optimal results.

3.3. Length of Credit History

- Importance: Accounts for 15% of your FICO score.

- Impact: A longer credit history generally indicates a more predictable borrowing pattern.

- Tips: Avoid closing old credit accounts, even if you don’t use them regularly.

3.4. Credit Mix

- Importance: Contributes 10% to your FICO score.

- Impact: Having a mix of credit accounts (e.g., credit cards, installment loans, mortgages) demonstrates your ability to manage different types of credit.

- Tips: Diversify your credit portfolio responsibly, without overextending yourself.

3.5. New Credit

- Importance: Accounts for 10% of your FICO score.

- Impact: Opening too many new credit accounts in a short period can lower your score, as it may indicate financial instability.

- Tips: Apply for new credit only when necessary.

3.6. VantageScore Factors

VantageScore also considers similar factors, but with slightly different emphasis:

- Payment History: Extremely influential.

- Total Credit Usage: Highly influential.

- Credit Mix and Experience: Highly influential.

- New Accounts Opened: Moderately influential.

- Balances and Available Credit: Less influential.

4. Improving Your Credit Score: Practical Steps

Improving your credit score takes time and discipline. Here are some actionable strategies:

4.1. Pay Bills on Time

- Action: Make all payments on time, every time.

- Tools: Set up automatic payments or reminders to avoid missed deadlines.

- Impact: Consistent on-time payments are the cornerstone of a good credit score.

4.2. Reduce Credit Utilization

- Action: Keep your credit utilization below 30%.

- Strategies: Pay down balances, request credit limit increases, or open a new credit card (responsibly).

- Impact: Lowering credit utilization demonstrates responsible credit management.

4.3. Monitor Your Credit Report

- Action: Regularly check your credit report for errors or inaccuracies.

- Resources: Obtain free credit reports from AnnualCreditReport.com.

- Impact: Identifying and correcting errors can improve your credit score.

4.4. Avoid Opening Too Many New Accounts

- Action: Apply for new credit only when necessary.

- Considerations: Each application can trigger a hard inquiry, potentially lowering your score.

- Impact: Limiting new accounts demonstrates financial stability.

4.5. Maintain a Healthy Credit Mix

- Action: Diversify your credit portfolio responsibly.

- Options: Consider a mix of credit cards, installment loans, and other credit products.

- Impact: A healthy credit mix showcases your ability to manage different types of credit.

5. Credit Scores and Major Purchases

Your credit score plays a significant role in major financial decisions, such as buying a house or a car.

5.1. Buying a House

- Mortgage Rates: A higher credit score can secure lower mortgage rates, saving you thousands over the life of the loan.

- Approval Odds: A good credit score increases your chances of mortgage approval.

- Minimum Scores: Some loan programs have minimum credit score requirements (e.g., FHA loans, VA loans).

5.2. Buying a Car

- Auto Loan Rates: Similar to mortgages, a better credit score can result in lower auto loan rates.

- Loan Terms: Lenders may offer more favorable loan terms to borrowers with good credit.

- Approval Odds: A decent credit score increases your chances of auto loan approval.

Average Mortgage Rates Based on FICO® Score

| FICO® Score | Interest Rate, 30-Year Fixed-Rate Mortgage | Monthly Payment | Total Interest Cost |

|---|---|---|---|

| 620 | 7.71% | $2,806.11 | $549,199 |

| 700 | 7.13% | $2,667.53 | $499,310 |

| 840 | 6.69% | $2,564.49 | $462,214 |

Source: Curinos LLC, December 6, 2024; assumes a $350,000 mortgage and 30-day rate-lock period

6. What to Do If You Have a Low Credit Score

If your credit score is low, don’t despair. There are steps you can take to improve it:

6.1. Identify the Issues

- Action: Review your credit report to identify the negative factors impacting your score.

- Common Issues: Late payments, high credit utilization, collections, bankruptcies.

6.2. Dispute Errors

- Action: Dispute any inaccuracies or errors on your credit report.

- Process: Contact the credit bureaus and provide documentation to support your claim.

6.3. Focus on Payment History and Credit Utilization

- Strategy: Prioritize making on-time payments and reducing credit utilization.

- Impact: These two factors have the most significant impact on your credit score.

6.4. Consider Secured Credit Cards

- Option: If you have difficulty qualifying for traditional credit cards, consider a secured credit card.

- How it Works: You provide a security deposit, which serves as your credit limit.

- Benefit: Responsible use can help you build or rebuild your credit.

6.5. Be Patient

- Reality: Improving your credit score takes time and consistency.

- Focus: Stay committed to responsible credit habits, and you’ll see results over time.

7. Common Misconceptions About Credit Scores

There are several common misconceptions about credit scores. Let’s debunk some of them:

7.1. Checking Your Credit Score Lowers It

- Reality: Checking your own credit score (using a soft inquiry) does not lower your score.

- Difference: Only hard inquiries (e.g., when applying for credit) can potentially impact your score.

7.2. Closing Accounts Improves Your Score

- Reality: Closing old credit accounts can actually lower your score, especially if they have a long credit history.

- Impact: Keeping accounts open (even if you don’t use them) can increase your available credit and improve your credit utilization ratio.

7.3. All Credit Scores Are the Same

- Reality: There are different credit scoring models (FICO and VantageScore) and different versions of each model.

- Variation: Your credit score may vary depending on the model and the data used.

7.4. Income Affects Your Credit Score

- Reality: Your income is not a direct factor in calculating your credit score.

- Focus: Credit scores are based on your credit history and payment behavior.

7.5. Paying Off a Loan Always Improves Your Score

- Reality: While paying off a loan is generally positive, it can sometimes lead to a temporary score drop.

- Reason: If it was your only installment loan, it could affect your credit mix.

8. The Future of Credit Scoring

The credit scoring landscape is constantly evolving, with new models and technologies emerging.

8.1. Trended Data

- Definition: Trended data considers your credit behavior over time, rather than just a snapshot.

- Impact: It provides a more comprehensive view of your creditworthiness.

8.2. Alternative Data

- Definition: Alternative data includes non-traditional sources of information, such as utility payments and rental history.

- Potential: It can help individuals with limited credit history establish creditworthiness.

8.3. AI and Machine Learning

- Application: AI and machine learning are being used to develop more sophisticated credit scoring models.

- Benefit: These models can potentially predict credit risk more accurately.

9. Maintaining Good Credit: A Long-Term Strategy

Building and maintaining a decent credit score is not a one-time task but an ongoing commitment to responsible financial habits.

9.1. Set Financial Goals

- Motivation: Having clear financial goals (e.g., buying a house, starting a business) can motivate you to maintain good credit.

9.2. Create a Budget

- Control: A budget helps you manage your finances and avoid overspending.

- Benefit: It ensures you have enough funds to pay your bills on time.

9.3. Monitor Your Credit Regularly

- Awareness: Stay informed about your credit score and credit report.

- Action: Address any issues promptly to prevent them from impacting your score.

9.4. Educate Yourself

- Knowledge: Understand the factors that influence your credit score and how to manage credit responsibly.

- Resources: Utilize reputable sources of information, such as WHAT.EDU.VN.

10. Frequently Asked Questions (FAQs) About Credit Scores

| Question | Answer |

|---|---|

| What is the lowest credit score? | The lowest credit score is 300, according to both the FICO and VantageScore models. |

| What is a good credit score range? | A good credit score typically falls between 670 and 739 on the FICO scale, or 661 and 780 according to VantageScore. |

| How can I check my credit score for free? | You can check your credit report for free annually at AnnualCreditReport.com. Some credit card companies and financial institutions also offer free credit score monitoring services. |

| Does closing a credit card account hurt my credit score? | Yes, closing a credit card account can hurt your credit score, particularly if it reduces your overall available credit or if the account has a long and positive credit history. |

| How long does it take to improve my credit score? | The time it takes to improve your credit score varies, but typically it can range from a few months to a year or more, depending on the specific actions you take and the current state of your credit. |

| What factors affect my credit score? | Factors that affect your credit score include payment history, amounts owed, length of credit history, credit mix, and new credit. |

| Is it better to have a high or low credit utilization ratio? | It is better to have a low credit utilization ratio, ideally below 30%. A high credit utilization ratio indicates that you are using a large portion of your available credit, which can negatively affect your credit score. |

| How do I dispute errors on my credit report? | To dispute errors on your credit report, contact the credit bureau that issued the report. Provide them with a detailed letter explaining the error and any supporting documentation. |

| Can I get a loan with a fair credit score? | Yes, it is possible to get a loan with a fair credit score (580-669), but you may face higher interest rates and less favorable terms compared to someone with a good or excellent credit score. |

| Does my income affect my credit score? | No, your income does not directly affect your credit score. Credit scores are based on your credit history, not your income. |

Remember, a decent credit score is within reach with consistent effort and responsible financial habits. Take control of your credit today and unlock a world of financial opportunities.

Do you have more questions about credit scores or personal finance? Visit WHAT.EDU.VN to ask your questions and receive free answers from our community of experts.

Address: 888 Question City Plaza, Seattle, WA 98101, United States

Whatsapp: +1 (206) 555-7890

Website: what.edu.vn

Don’t hesitate, ask your question now and get the answers you need!