What Is A High Credit Score? It’s your key to unlocking better financial opportunities. At WHAT.EDU.VN, we understand the importance of a strong credit rating. We provide simple explanations, actionable advice, and free resources to help you achieve excellent credit and secure your financial future. Discover credit score ranges and creditworthiness insights.

1. Understanding Credit Scores: An Overview

A credit score is a three-digit number that reflects your creditworthiness, based on your credit history. Lenders use this score to determine the risk of lending you money. A higher score generally means you are a lower-risk borrower, which can lead to better interest rates and loan terms. There are two main credit scoring models: FICO and VantageScore.

-

FICO Score: This is the most widely used credit scoring model, used by the majority of lenders. FICO scores range from 300 to 850.

-

VantageScore: This is a competing model developed by the three major credit bureaus: Experian, TransUnion, and Equifax. VantageScore also ranges from 300 to 850.

Both FICO and VantageScore consider similar factors when calculating your credit score, but they may weigh these factors differently.

2. What is Considered a High Credit Score?

A high credit score indicates that you have a history of responsible credit use. Generally, a score of 700 or above is considered good, but to truly be considered a high credit score, you should aim for the upper ranges.

-

FICO Score Ranges:

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

-

VantageScore Ranges:

- Excellent: 781-850

- Good: 661-780

- Fair: 601-660

- Poor: 300-600

Aiming for a score in the “Very Good” or “Exceptional” range will provide you with the most benefits, such as lower interest rates and better loan terms.

3. Benefits of Having a High Credit Score

A high credit score can significantly impact your financial life in many positive ways. Here are some key benefits:

-

Lower Interest Rates: With a high credit score, you’re more likely to qualify for lower interest rates on loans and credit cards. This can save you thousands of dollars over the life of a loan.

-

Better Loan Terms: Lenders offer more favorable terms, such as longer repayment periods and lower fees, to borrowers with high credit scores.

-

Increased Approval Odds: Whether you’re applying for a mortgage, auto loan, or credit card, a high credit score increases your chances of being approved.

-

Higher Credit Limits: Credit card companies are more likely to offer higher credit limits to individuals with high credit scores, providing greater purchasing power and flexibility.

-

Negotiating Power: A high credit score gives you leverage to negotiate better deals with lenders and service providers.

-

Easier Apartment Rentals: Landlords often check credit scores as part of the application process. A high score can make it easier to rent an apartment or home.

-

Lower Insurance Premiums: In many states, insurance companies use credit-based insurance scores to determine premiums. A high credit score can result in lower auto, home, and life insurance rates.

-

Utility and Phone Service Approvals: Utility companies and phone service providers may check your credit before approving your application. A high score can help you avoid security deposits and get approved more easily.

-

Employment Opportunities: Some employers check credit reports (but not scores) as part of their hiring process. A responsible credit history can make you a more attractive candidate.

4. Factors That Influence Your Credit Score

Understanding the factors that influence your credit score is crucial for maintaining and improving it. The main factors include:

-

Payment History (35% of FICO Score): This is the most important factor. It reflects whether you’ve made past credit payments on time. Late payments, collections, and bankruptcies can significantly lower your score.

-

Amounts Owed (30% of FICO Score): This refers to the total amount of debt you owe and your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (below 30%) can help improve your score.

-

Length of Credit History (15% of FICO Score): A longer credit history generally leads to a higher score. Lenders want to see a track record of responsible credit use over time.

-

Credit Mix (10% of FICO Score): Having a mix of different types of credit, such as credit cards, installment loans, and mortgages, can positively impact your score.

-

New Credit (10% of FICO Score): Opening too many new accounts in a short period can lower your score, as it may indicate higher risk.

5. Practical Steps to Achieve a High Credit Score

Improving your credit score requires consistent effort and responsible financial habits. Here are some practical steps you can take:

-

Pay Bills on Time: Always pay your bills by the due date. Set up reminders or automatic payments to avoid late payments.

-

Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on each credit card. For example, if you have a credit card with a $1,000 limit, try to keep your balance below $300.

-

Monitor Your Credit Reports: Check your credit reports regularly for errors or fraudulent activity. You can get a free copy of your credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) annually at AnnualCreditReport.com.

-

Avoid Opening Too Many New Accounts: Opening multiple new accounts in a short period can lower your score. Be selective about applying for new credit.

-

Maintain a Mix of Credit Accounts: Having a variety of credit accounts, such as credit cards, installment loans, and a mortgage, can demonstrate responsible credit management.

-

Become an Authorized User: If you have a family member or friend with a credit card and a good credit history, ask if you can become an authorized user on their account. Their positive credit history can help improve your credit score.

-

Consider a Secured Credit Card: If you have poor credit or no credit history, a secured credit card can be a good way to build credit. These cards require a cash deposit as collateral, which also serves as your credit limit.

6. Common Misconceptions About Credit Scores

There are several common misconceptions about credit scores that can lead to confusion and poor financial decisions. Here are a few to keep in mind:

-

Checking Your Own Credit Score Will Lower It: This is false. Checking your own credit score is considered a “soft inquiry” and does not affect your credit score.

-

Closing Credit Cards Will Improve Your Score: Closing credit cards can actually lower your score, especially if they have a high credit limit and you carry balances on other cards. This is because it reduces your overall available credit and increases your credit utilization ratio.

-

Credit Scores Only Matter for Loans: Credit scores are used for much more than just loans. They can affect your ability to rent an apartment, get insurance, and even get a job.

-

All Credit Scores Are the Same: There are many different credit scoring models and versions, and your score can vary depending on the model and the credit bureau used.

-

You Need to Carry a Balance to Build Credit: This is not true. You can build credit by using your credit card for small purchases and paying the balance in full each month.

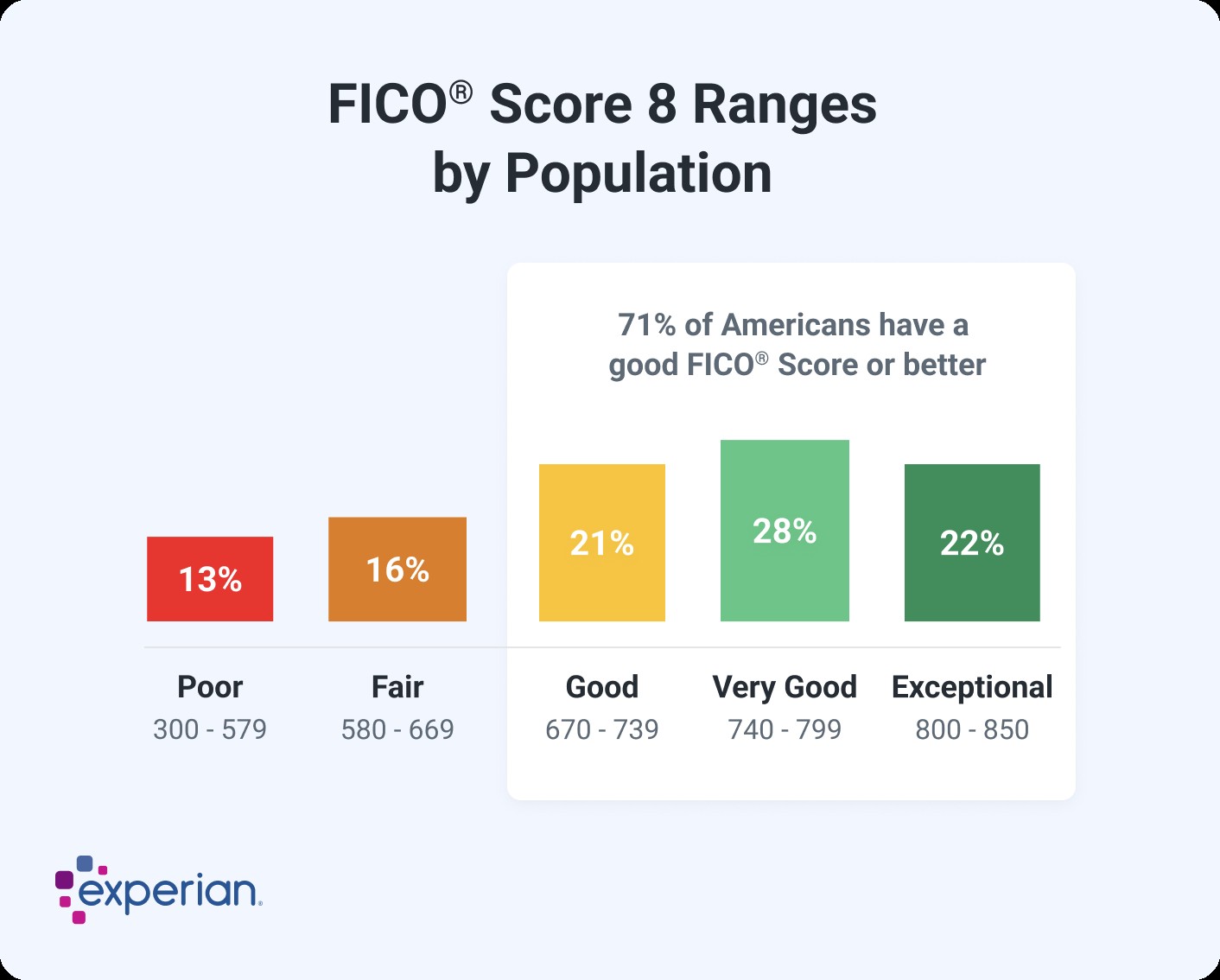

7. Credit Score Ranges: A Detailed Breakdown

Understanding the different credit score ranges can help you assess your credit health and set goals for improvement. Here’s a detailed breakdown of the FICO and VantageScore ranges:

-

FICO Score Ranges:

- 800-850 (Exceptional): This is the highest credit score range, indicating excellent credit management. Borrowers in this range qualify for the best interest rates and loan terms.

- 740-799 (Very Good): This range indicates a strong credit history. Borrowers in this range are likely to be approved for most loans and credit cards with favorable terms.

- 670-739 (Good): This range is considered average to good. Borrowers in this range are generally approved for loans and credit cards, but may not receive the best interest rates.

- 580-669 (Fair): This range indicates a credit history with some issues. Borrowers in this range may have difficulty getting approved for loans and credit cards, or may receive higher interest rates.

- 300-579 (Poor): This is the lowest credit score range, indicating a history of significant credit problems. Borrowers in this range are likely to be denied credit or receive very high interest rates.

-

VantageScore Ranges:

- 781-850 (Excellent): Similar to the FICO “Exceptional” range, this indicates excellent credit management.

- 661-780 (Good): This range is roughly equivalent to the FICO “Good” and “Very Good” ranges, indicating a solid credit history.

- 601-660 (Fair): This range is similar to the FICO “Fair” range, indicating some credit challenges.

- 300-600 (Poor): This is the lowest VantageScore range, indicating significant credit problems.

8. How to Monitor Your Credit Score for Free

Monitoring your credit score regularly is essential for tracking your progress and identifying any potential issues. Here are several ways to monitor your credit score for free:

-

AnnualCreditReport.com: As mentioned earlier, you can get a free copy of your credit report from each of the three major credit bureaus annually. While this doesn’t provide your credit score, it allows you to review your credit history for errors.

-

Credit Karma: Credit Karma provides free credit scores and reports based on the VantageScore 3.0 model. It also offers credit monitoring and personalized recommendations for improving your credit.

-

Credit Sesame: Credit Sesame offers free credit scores, reports, and credit monitoring services. It also provides tools for managing your debt and improving your credit.

-

Experian: Experian offers a free credit score and report, as well as credit monitoring and alerts for suspicious activity.

-

Discover Credit Scorecard: If you’re not a Discover cardholder, you can still use Discover’s Credit Scorecard to get a free FICO score and credit report summary.

-

Your Credit Card Company: Many credit card companies offer free credit scores to their cardholders as a benefit. Check your credit card statement or online account to see if this is available.

-

Free Financial Counseling: Non-profit credit counseling agencies often provide free credit score reviews and advice on improving your credit.

9. What to Do If You Find Errors on Your Credit Report

Finding errors on your credit report is more common than you might think. These errors can negatively impact your credit score, so it’s important to address them promptly. Here’s what to do:

-

Obtain Your Credit Reports: Get a copy of your credit reports from all three major credit bureaus.

-

Identify the Errors: Carefully review each report and highlight any inaccuracies, such as incorrect account balances, late payments that were actually made on time, or accounts that don’t belong to you.

-

Gather Supporting Documentation: Collect any documents that support your claim, such as bank statements, payment confirmations, and correspondence with creditors.

-

File a Dispute with the Credit Bureau: Write a letter to each credit bureau where you found errors, explaining the inaccuracies and providing copies of your supporting documents. You can also file a dispute online through the credit bureau’s website.

- Experian: https://www.experian.com/

- TransUnion: https://www.transunion.com/

- Equifax: https://www.equifax.com/

-

Contact the Creditor: If the error involves an account with a specific creditor, contact them directly to dispute the information.

-

Follow Up: The credit bureau has 30 days to investigate your dispute. They will contact the creditor to verify the information. If the error is verified, the credit bureau will update your credit report.

-

Review the Results: Once the investigation is complete, the credit bureau will send you the results. Review the updated credit report to ensure that the errors have been corrected.

-

If the Error Persists: If the credit bureau does not correct the error, you have the right to add a statement to your credit report explaining the dispute.

10. Building Credit When Starting from Scratch

Building credit from scratch can seem daunting, but it’s entirely achievable with the right strategies. Here are some steps to get started:

-

Become an Authorized User: As mentioned earlier, becoming an authorized user on a credit card account with a positive credit history can help you build credit.

-

Apply for a Secured Credit Card: Secured credit cards are designed for people with no credit history or poor credit. They require a cash deposit as collateral, which also serves as your credit limit. Use the card responsibly and pay your balance on time each month to build credit.

-

Consider a Credit-Builder Loan: These loans are specifically designed to help people build credit. You borrow a small amount of money, and the lender reports your payments to the credit bureaus.

-

Apply for a Retail Credit Card: Retail credit cards, also known as store cards, are often easier to get approved for than traditional credit cards. Use the card for purchases at the store and pay your balance on time each month.

-

Report Rent and Utility Payments: Some credit reporting services allow you to report your rent and utility payments to the credit bureaus. This can help you build credit by demonstrating a history of on-time payments.

-

Be Patient and Consistent: Building credit takes time and consistent effort. Stay patient and continue to use credit responsibly to see results.

11. How a High Credit Score Affects Mortgage Rates

Your credit score plays a significant role in determining the interest rate you’ll receive on a mortgage. Lenders use your credit score to assess the risk of lending you money. A higher credit score indicates that you’re a lower-risk borrower, which can result in a lower interest rate.

Here’s how a high credit score can affect your mortgage rate:

-

Lower Interest Rates: Borrowers with high credit scores typically qualify for the lowest interest rates. This can save you thousands of dollars over the life of the loan.

-

Better Loan Terms: Lenders may offer more favorable terms, such as lower fees and more flexible repayment options, to borrowers with high credit scores.

-

Increased Approval Odds: A high credit score increases your chances of being approved for a mortgage, especially if you have a limited credit history or a high debt-to-income ratio.

-

Larger Loan Amounts: Lenders may be willing to lend you more money if you have a high credit score, as they view you as a lower-risk borrower.

The difference in mortgage rates between borrowers with high and low credit scores can be significant. For example, a borrower with a FICO score of 760 or higher may receive an interest rate that is 0.5% to 1% lower than a borrower with a FICO score below 620. On a $300,000 mortgage, this could save you tens of thousands of dollars over the life of the loan.

12. Impact of Credit Scores on Auto Loan Rates

Similar to mortgages, your credit score also affects the interest rate you’ll receive on an auto loan. Lenders use your credit score to assess the risk of lending you money for a car purchase.

Here’s how a high credit score can impact your auto loan rate:

-

Lower Interest Rates: Borrowers with high credit scores typically qualify for the lowest interest rates on auto loans.

-

Better Loan Terms: Lenders may offer more favorable terms, such as lower monthly payments and shorter loan terms, to borrowers with high credit scores.

-

Increased Approval Odds: A high credit score increases your chances of being approved for an auto loan, especially if you have a limited credit history or a high debt-to-income ratio.

The difference in auto loan rates between borrowers with high and low credit scores can be substantial. According to Experian, the average interest rate for borrowers with a credit score of 781-850 was significantly lower than the rate for borrowers with a credit score of 501-600. This can save you hundreds or even thousands of dollars over the life of the loan.

13. Credit Scores and Credit Cards: Maximizing Benefits

Your credit score plays a crucial role in your ability to get approved for credit cards and the terms you’ll receive. A high credit score can unlock a variety of benefits when it comes to credit cards.

Here are some ways to maximize the benefits of having a high credit score when using credit cards:

-

Qualify for Premium Rewards Cards: Credit cards with the best rewards programs, such as travel rewards, cash back, and points, typically require a high credit score for approval.

-

Receive Lower Interest Rates: Credit card companies offer lower interest rates to borrowers with high credit scores. This can save you money on interest charges if you carry a balance on your card.

-

Get Higher Credit Limits: A high credit score can help you get approved for credit cards with higher credit limits, providing greater purchasing power and flexibility.

-

Take Advantage of 0% APR Offers: Many credit cards offer 0% APR promotional periods for purchases or balance transfers. A high credit score can increase your chances of being approved for these offers, allowing you to save money on interest charges.

-

Negotiate Better Terms: If you already have a credit card, you may be able to negotiate better terms, such as a lower interest rate or higher credit limit, by demonstrating that you have a high credit score.

14. Credit Score Myths Debunked

It’s important to separate fact from fiction when it comes to credit scores. Here are some common credit score myths debunked:

-

Myth: Checking your own credit score will lower it.

- Fact: Checking your own credit score is considered a “soft inquiry” and does not affect your credit score.

-

Myth: Closing credit cards will improve your score.

- Fact: Closing credit cards can actually lower your score, especially if they have a high credit limit and you carry balances on other cards.

-

Myth: Credit scores only matter for loans.

- Fact: Credit scores are used for much more than just loans. They can affect your ability to rent an apartment, get insurance, and even get a job.

-

Myth: All credit scores are the same.

- Fact: There are many different credit scoring models and versions, and your score can vary depending on the model and the credit bureau used.

-

Myth: You need to carry a balance to build credit.

- Fact: You can build credit by using your credit card for small purchases and paying the balance in full each month.

15. Maintaining a High Credit Score Over Time

Achieving a high credit score is a great accomplishment, but it’s important to maintain it over time. Here are some tips for maintaining a high credit score:

-

Continue to Pay Bills on Time: Always pay your bills by the due date, even if it’s just the minimum payment.

-

Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on each credit card.

-

Monitor Your Credit Reports Regularly: Check your credit reports for errors or fraudulent activity.

-

Avoid Opening Too Many New Accounts: Be selective about applying for new credit.

-

Maintain a Mix of Credit Accounts: Having a variety of credit accounts can demonstrate responsible credit management.

-

Be Patient and Consistent: Maintaining a high credit score takes time and consistent effort.

16. The Role of Credit Utilization in Achieving a High Score

Credit utilization is a critical factor in determining your credit score. It refers to the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low can significantly improve your credit score.

Here’s why credit utilization is so important:

-

It’s a Significant Factor: Credit utilization accounts for 30% of your FICO score, making it one of the most important factors.

-

It Shows Responsible Credit Management: Keeping your credit utilization low demonstrates that you’re using credit responsibly and not overextending yourself.

-

It Can Improve Your Score Quickly: Lowering your credit utilization can have a positive impact on your credit score in a relatively short period of time.

Here are some tips for keeping your credit utilization low:

-

Keep Balances Low: Aim to keep your credit card balances as low as possible.

-

Pay Off Balances Regularly: Pay off your credit card balances in full each month, or at least make more than the minimum payment.

-

Increase Credit Limits: If possible, ask your credit card company to increase your credit limit. This will lower your credit utilization ratio, even if you don’t spend more money.

-

Use Multiple Credit Cards: If you have multiple credit cards, spread your spending across them to keep the utilization low on each card.

17. How to Use Credit Wisely to Build and Maintain a High Score

Using credit wisely is essential for building and maintaining a high credit score. Here are some tips for using credit responsibly:

-

Only Borrow What You Can Afford: Before taking on any debt, make sure you can comfortably afford the monthly payments.

-

Pay Bills on Time: Always pay your bills by the due date, even if it’s just the minimum payment.

-

Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on each credit card.

-

Avoid Maxing Out Credit Cards: Maxing out your credit cards can damage your credit score and make it difficult to pay off your debt.

-

Monitor Your Credit Reports Regularly: Check your credit reports for errors or fraudulent activity.

-

Avoid Opening Too Many New Accounts: Be selective about applying for new credit.

-

Use Credit for Necessary Purchases: Use credit for necessary purchases, such as a car or a home, rather than for discretionary spending.

18. Building a High Credit Score as a Student

Building credit as a student can set you up for financial success in the future. Here are some tips for building credit as a student:

-

Apply for a Student Credit Card: Many credit card companies offer credit cards specifically designed for students. These cards often have lower credit limits and easier approval requirements.

-

Become an Authorized User: Ask a parent or family member if you can become an authorized user on their credit card account.

-

Use Credit for Small Purchases: Use your credit card for small purchases, such as gas or groceries, and pay the balance in full each month.

-

Pay Bills on Time: Always pay your bills by the due date, even if it’s just the minimum payment.

-

Avoid Maxing Out Credit Cards: Maxing out your credit cards can damage your credit score and make it difficult to pay off your debt.

-

Monitor Your Credit Reports Regularly: Check your credit reports for errors or fraudulent activity.

19. Strategies for Recovering from a Low Credit Score

Recovering from a low credit score takes time and effort, but it’s definitely possible. Here are some strategies for improving your credit score:

-

Pay Bills on Time: Make all of your payments on time, every time. Set up reminders or automatic payments to avoid late payments.

-

Reduce Debt: Pay down your existing debt as quickly as possible. Focus on paying off high-interest debt first.

-

Keep Credit Utilization Low: Aim to use no more than 30% of your available credit on each credit card.

-

Monitor Your Credit Reports Regularly: Check your credit reports for errors or fraudulent activity.

-

Dispute Errors: If you find any errors on your credit reports, dispute them with the credit bureaus.

-

Consider a Secured Credit Card: Secured credit cards can help you rebuild credit by reporting your payments to the credit bureaus.

-

Be Patient: Improving your credit score takes time. Stay patient and continue to use credit responsibly to see results.

20. Expert Tips for Managing and Improving Your Credit Score

Here are some expert tips for managing and improving your credit score:

-

Treat Your Credit Score Like a Financial Asset: Your credit score is a valuable financial asset. Protect it by using credit responsibly and monitoring your credit reports regularly.

-

Focus on the Factors You Can Control: You can’t change the past, but you can control your future credit behavior. Focus on paying bills on time, keeping credit utilization low, and avoiding new debt.

-

Seek Professional Help if Needed: If you’re struggling to manage your debt or improve your credit score, consider seeking help from a non-profit credit counseling agency.

-

Be Wary of Credit Repair Scams: Be cautious of companies that promise to “fix” your credit score quickly. These companies are often scams and may charge you exorbitant fees for services that you can do yourself.

-

Stay Informed: Stay informed about credit scores and credit management. The more you know, the better equipped you’ll be to make smart financial decisions.

We hope this comprehensive guide has provided you with a clear understanding of what constitutes a high credit score and how to achieve it. Remember, building and maintaining a high credit score requires consistent effort and responsible financial habits.

Do you have questions about your credit score or need help improving it? Visit what.edu.vn today and ask your question for free. Our community of experts is ready to provide you with the answers and support you need to achieve your financial goals. Don’t wait, take control of your credit score today. Contact us at 888 Question City Plaza, Seattle, WA 98101, United States. Whatsapp: +1 (206) 555-7890.