EChecks, also known as electronic checks, are revolutionizing payment methods in today’s digital world. Learn more about eChecks with WHAT.EDU.VN, including their functionality, benefits, and security aspects. Find out how eChecks can streamline your transactions and offer a secure alternative to traditional paper checks. Discover key insights into electronic fund transfers and digital payments.

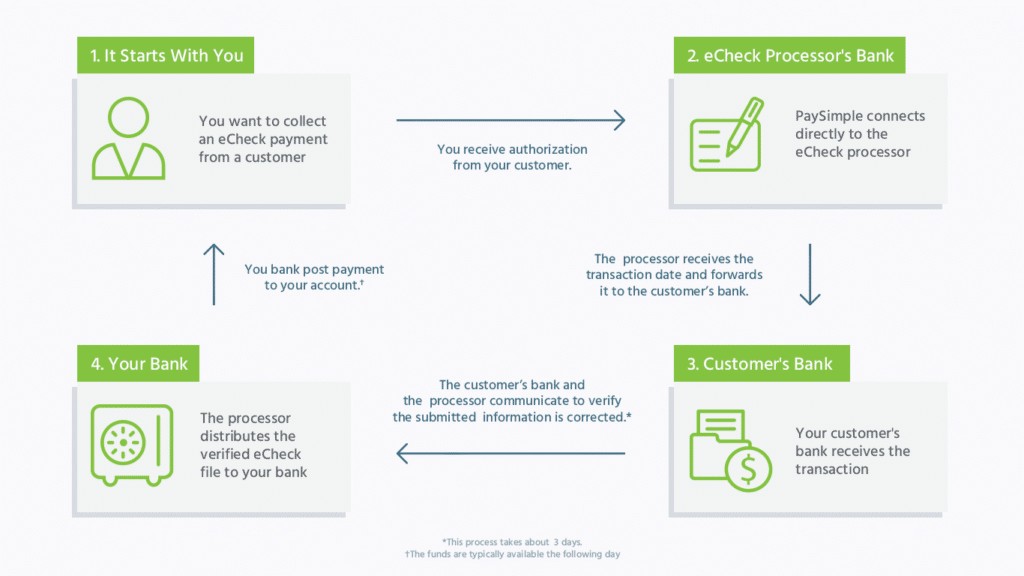

An eCheck, short for electronic check, is a digital form of a traditional paper check. Instead of physically writing and mailing a check, an eCheck allows you to transfer money electronically from your checking account to another party’s account. This process occurs over the Automated Clearing House (ACH) network, a U.S. financial institution network.

Think of it as paying with a paper check but without the paper. You provide your bank account details (routing and account number) to the merchant or payee, who then initiates the transfer electronically.

eCheck concept with digital check image and financial symbols

eCheck concept with digital check image and financial symbols

2. How Does an eCheck Work?

The magic of eChecks lies in their simplicity and efficiency. Here’s a breakdown of the process:

- Authorization: First, you need to authorize the merchant or payee to debit your account. This can be done through a signed agreement, a website’s terms and conditions, or even a recorded phone conversation.

- Information Submission: Once authorized, you provide your bank account’s routing number and account number to the merchant. This information is securely entered into their payment processing system.

- ACH Transfer: The merchant then uses this information to initiate an ACH transfer. The ACH network acts as the intermediary, verifying the information and moving the funds.

- Funds Transfer: The money is electronically withdrawn from your account and deposited into the merchant’s account.

- Confirmation: Both you and the merchant receive confirmation of the transaction.

The entire process typically takes between three to five business days.

3. What are the Benefits of Using eChecks?

eChecks offer a range of advantages over traditional paper checks and other payment methods:

- Convenience: No more writing, mailing, or physically depositing checks. Everything is done electronically.

- Speed: eChecks are generally faster than paper checks, with funds typically clearing in a few business days.

- Security: eChecks offer robust security measures to protect your financial information. The ACH network employs encryption and fraud detection systems.

- Cost-Effectiveness: eCheck processing fees are often lower than credit card processing fees, making them an attractive option for businesses.

- Environmentally Friendly: By eliminating paper checks, eChecks contribute to a greener environment.

- Recurring Payments: eChecks are ideal for setting up recurring payments, such as rent, utilities, or subscriptions.

4. What Information is Needed to Pay With an eCheck?

Paying with an eCheck requires only a few key pieces of information:

- Bank Name: The name of your financial institution.

- Routing Number: A nine-digit code that identifies your bank.

- Account Number: Your specific checking account number.

- Payment Amount: The amount you wish to pay.

- Authorization: Your explicit permission for the merchant to debit your account.

5. How Secure Are eChecks?

eChecks are a very secure method of payment, offering several layers of protection:

- ACH Security: The ACH network itself has security protocols in place, including encryption and fraud detection systems.

- Authorization Requirements: Merchants must obtain your authorization before initiating an eCheck payment.

- Data Encryption: Reputable payment processors use encryption to protect your bank account information during transmission and storage.

- Fraud Monitoring: Many banks and payment processors offer fraud monitoring services to detect and prevent unauthorized transactions.

It is crucial to use trusted and reputable payment processors when using eChecks to minimize risks.

6. What is the Difference Between eCheck, ACH, and EFT?

These terms are often used interchangeably, but there are subtle differences:

- EFT (Electronic Funds Transfer): This is the broadest term, encompassing any electronic transfer of money, including wire transfers, direct deposits, and ACH transfers.

- ACH (Automated Clearing House): This refers to the electronic network used by U.S. financial institutions to process electronic payments, including eChecks.

- eCheck (Electronic Check): This is a specific type of EFT that utilizes the ACH network to debit a checking account electronically.

In essence, an eCheck is a specific type of EFT that relies on the ACH network for processing.

7. What Types of Payments Can I Make With an eCheck?

EChecks are versatile and can be used for a wide range of payments, including:

- Online Purchases: Many online retailers accept eChecks as a payment option.

- Bill Payments: Pay your utility bills, credit card bills, and other recurring expenses with eChecks.

- Rent Payments: Landlords often accept eChecks for rent payments.

- Mortgage Payments: Some mortgage lenders allow you to make your payments via eCheck.

- Business Transactions: Businesses can use eChecks to pay vendors, suppliers, and employees.

- Donations: Many non-profit organizations accept eCheck donations.

8. Can I Use eChecks for Recurring Payments?

Absolutely. EChecks are an excellent choice for recurring payments. You can set up automatic payments for subscriptions, memberships, loans, and other recurring expenses. This eliminates the need to manually pay each month and ensures that your payments are always on time.

Property managers frequently use eChecks to collect rent payments automatically each month.

9. How Long Does it Take for an eCheck to Clear?

The processing time for eChecks typically ranges from three to five business days. This timeframe allows for verification of funds availability and processing through the ACH network. While faster than traditional paper checks, it’s important to factor in this processing time when making payments.

10. How Do I Send an eCheck Payment?

To send an eCheck payment, you’ll typically need to provide the following information to the payee:

- Payee Information: Confirm that the recipient accepts eCheck payments and has an ACH merchant account.

- Bank Details: Your bank name, routing number, and account number.

- Authorization: Grant permission for the payee to debit your account for the specified amount.

- Online Payment Form: The payee usually provides an online form to securely enter your banking details.

- Phone Authorization: In some cases, you can provide your information and authorization over a recorded phone call.

11. Do eChecks Process on Weekends?

Since eChecks rely on the ACH network and financial institutions, processing is typically limited to business days. Payments authorized on weekends or holidays will begin processing on the next business day. This means that if you make a payment on Friday, the funds may not be debited from your account until the following week.

12. What Happens If an eCheck Bounces?

If an eCheck bounces due to insufficient funds in your account, it’s essential to address the issue promptly. Here’s what typically happens:

- Notification: You’ll receive a notification from your bank or the payee that the eCheck has been returned.

- Fees: Your bank may charge you a fee for the bounced eCheck, and the payee may also assess a returned payment fee.

- Payment Arrangement: Contact the payee immediately to arrange an alternative payment method.

- Late Payment Penalties: Failure to resolve the bounced eCheck promptly may result in late payment penalties or other consequences.

13. How Do I Cancel an eCheck?

Canceling an eCheck depends on the stage of the transaction.

- Pending Transactions: If the payment is still pending, contact your payment processor or bank immediately to request a cancellation. They may be able to stop the payment before it is processed.

- Cleared Transactions: If the payment has already cleared, you cannot cancel the eCheck. You’ll need to request a refund from the payee.

- Payment System Policies: The exact cancellation procedure will depend on the specific payment system you’re using. Check their policies or contact their customer support for assistance.

14. How Much Does It Cost to Process an eCheck?

The cost of processing an eCheck varies depending on the payment processor and the specific agreement you have with them. Generally, eCheck processing fees are lower than credit card processing fees.

- Transaction Fees: eCheck processors typically charge a per-transaction fee, which can range from $0.30 to $1.50 per transaction.

- Monthly Fees: Some processors may also charge a monthly fee for using their service.

- Bundled Packages: Some providers offer bundled packages that include eCheck processing along with other payment processing services.

15. How Can I Get an eCheck Merchant Account for My Business?

To accept eCheck payments from your customers, you’ll need to set up an eCheck merchant account. Here’s how:

- Research Providers: Look for reputable payment processors that offer eCheck processing services.

- Application: Complete the application process, providing information about your business, such as your Federal Tax Identification Number (EIN), years in business, and estimated processing volumes.

- Underwriting: The payment processor will review your application and conduct an underwriting process to assess your risk.

- Approval: If approved, you’ll receive an eCheck merchant account and can start accepting eCheck payments from your customers.

- Account Setup: The application process is similar to setting up a credit card merchant account.

16. What are Some Common eCheck Scams to Watch Out For?

While eChecks are generally secure, it’s essential to be aware of potential scams:

- Overpayment Scams: A scammer sends you an eCheck for more than the agreed-upon amount and asks you to refund the difference. The original eCheck may bounce, leaving you liable for the full amount.

- Phishing Scams: Scammers may send you emails or text messages pretending to be from a legitimate company, asking you to provide your bank account information to receive an eCheck payment.

- Fake Check Scams: Scammers may send you a fake eCheck as part of a fraudulent scheme, such as a lottery scam or a work-from-home scam.

17. How Can I Protect Myself From eCheck Fraud?

To protect yourself from eCheck fraud, follow these tips:

- Verify the Payee: Before providing your bank account information, verify the identity of the payee.

- Secure Websites: Only enter your bank account information on secure websites with HTTPS in the address bar.

- Don’t Overshare: Never share your bank account information with unsolicited callers or emails.

- Monitor Your Account: Regularly monitor your bank account for any unauthorized transactions.

- Report Suspicious Activity: If you suspect fraud, report it to your bank and the Federal Trade Commission (FTC).

18. What are the Alternatives to eChecks?

While eChecks offer many advantages, several alternatives are available:

- Credit Cards: Credit cards are a widely accepted payment method, offering convenience and purchase protection.

- Debit Cards: Debit cards allow you to make purchases directly from your bank account.

- Wire Transfers: Wire transfers are a fast and secure way to send money electronically, but they can be more expensive than eChecks.

- Payment Apps: Payment apps like PayPal, Venmo, and Zelle allow you to send and receive money electronically.

- Cryptocurrencies: Cryptocurrencies like Bitcoin offer a decentralized and secure way to make payments.

19. What is the Future of eChecks?

The future of eChecks looks promising. As more businesses and consumers embrace digital payments, eChecks are likely to become even more popular.

- Increased Adoption: Expect to see wider adoption of eChecks as more businesses recognize their cost-effectiveness and convenience.

- Technological Advancements: Advancements in technology are likely to make eCheck processing even faster and more secure.

- Integration with Mobile Wallets: EChecks may become integrated with mobile wallets, making them even more convenient to use.

- Global Expansion: While currently most popular in the U.S., eChecks may expand to other countries as digital payment adoption increases globally.

20. How Can WHAT.EDU.VN Help Me With My Questions About eChecks?

At WHAT.EDU.VN, we understand that navigating the world of digital payments can be confusing. That’s why we offer a free question and answer platform where you can get expert advice on eChecks and other financial topics.

Have questions about setting up an eCheck merchant account? Unsure about the security of eChecks? Our community of experts is here to help.

Don’t hesitate to ask your questions on WHAT.EDU.VN and get the answers you need to make informed decisions about your finances.

Tired of searching endlessly for answers? Visit WHAT.EDU.VN today and ask your question for free. Let our experts provide you with the clarity you need. Our services are always free, and we’re here to help you find the answers you’re looking for.

Need immediate answers? Contact us at:

Address: 888 Question City Plaza, Seattle, WA 98101, United States

WhatsApp: +1 (206) 555-7890

Website: WHAT.EDU.VN

FAQ: Frequently Asked Questions About eChecks

| Question | Answer |

|---|---|

| Are eChecks safe to use for online transactions? | Yes, when using reputable payment processors and taking precautions such as verifying the payee and using secure websites. |

| Can I dispute an eCheck transaction if I suspect fraud? | Yes, you can dispute an eCheck transaction with your bank if you suspect fraud. Contact your bank immediately and follow their dispute resolution process. |

| What happens if the sender cancels an eCheck after I’ve already provided the goods or services? | This can be a challenging situation. Contact your bank and legal counsel immediately. Depending on the circumstances, you may have legal recourse to recover the funds. |

| Is there a limit to the amount I can pay with an eCheck? | Some banks or payment processors may impose limits on the amount you can pay with an eCheck. Check with your bank or payment processor for details. |

| Can I use eChecks to make international payments? | While eChecks are primarily used for domestic transactions within the United States, some payment processors may offer international eCheck services. Check with your payment processor for availability and fees. |

| What are the legal regulations governing eCheck transactions? | ECheck transactions are governed by the Electronic Funds Transfer Act (EFTA) and other regulations. These laws protect consumers and businesses from fraud and unauthorized transactions. |

| How do I reconcile eCheck payments in my accounting software? | Most accounting software packages offer features to reconcile eCheck payments. You’ll need to match the eCheck transactions in your bank statement with the corresponding entries in your accounting software. |

| Are eChecks subject to sales tax? | Whether eChecks are subject to sales tax depends on the nature of the goods or services being purchased and the applicable state and local laws. Consult with a tax professional for guidance. |

| What is the difference between a personal eCheck and a business eCheck? | A personal eCheck is used for personal transactions, while a business eCheck is used for business transactions. Business eChecks may require additional information, such as the company’s EIN. |

| How can I track the status of an eCheck payment? | You can typically track the status of an eCheck payment through your online banking portal or by contacting your bank or payment processor. |

| What are the best practices for securing eCheck payments for my business? | Implement security measures such as using secure payment gateways, encrypting sensitive data, and monitoring for fraudulent activity. |

| How do I handle chargebacks or disputes related to eCheck payments? | Have a clear dispute resolution process in place and work with your payment processor to address chargebacks or disputes promptly. |

| What are the reporting requirements for eCheck transactions? | Businesses may be required to report eCheck transactions to the IRS or other government agencies. Consult with a tax professional for guidance. |

| How do I choose the right eCheck payment processor for my business? | Consider factors such as processing fees, security features, integration capabilities, and customer support when choosing an eCheck payment processor. |

| What are the common mistakes to avoid when using eChecks? | Avoid common mistakes such as entering incorrect bank account information, failing to authorize payments, and not monitoring your account for unauthorized transactions. |

| How are eChecks impacted by new regulations or laws in the financial industry? | Stay informed about changes in financial regulations or laws that may impact eCheck transactions. Consult with legal or financial professionals for guidance. |

| What is the role of blockchain technology in the future of eChecks? | Blockchain technology may offer opportunities to enhance the security and efficiency of eCheck transactions. |

| How do eChecks compare to other digital payment methods in terms of cost and security? | EChecks generally offer lower processing fees compared to credit cards and can be as secure or more secure than other digital payment methods when proper precautions are taken. |

| What is the impact of mobile payments on the adoption of eChecks? | Mobile payments are driving the adoption of eChecks by making it easier for consumers to make payments on the go. |

| How do I educate my customers about the benefits of using eChecks? | Communicate the benefits of using eChecks, such as convenience, security, and cost savings, to your customers through marketing materials and customer support. |

| What steps should I take if I suspect an eCheck payment is fraudulent or unauthorized? | Contact your bank or payment processor immediately, report the incident to law enforcement, and monitor your account for any further suspicious activity. |

| How can I ensure compliance with PCI DSS standards when processing eCheck payments? | Implement security measures such as encrypting sensitive data, restricting access to payment systems, and regularly monitoring for vulnerabilities to ensure compliance with PCI DSS standards. |

| What are the best practices for managing recurring eCheck payments? | Obtain proper authorization from customers, provide clear and transparent billing information, and offer easy options for canceling or modifying recurring payments. |

| How do I integrate eCheck payments into my existing accounting or ERP system? | Work with your accounting or ERP system provider to integrate eCheck payments seamlessly into your existing workflows. |

| What are the tax implications of accepting eCheck payments for my business? | Consult with a tax professional to understand the tax implications of accepting eCheck payments, such as reporting requirements and deductions. |

| How do I protect my business from chargebacks or disputes related to eCheck payments? | Implement fraud prevention measures, provide excellent customer service, and have a clear dispute resolution process in place to minimize the risk of chargebacks or disputes. |

| What are the future trends in eCheck technology and payment processing? | Stay informed about emerging trends such as real-time payments, blockchain technology, and mobile wallets, and consider how they may impact eCheck payments in the future. |

| How can I leverage eCheck payments to improve cash flow and reduce processing costs for my business? | Negotiate lower processing fees with your payment processor, encourage customers to pay with eChecks instead of credit cards, and automate your payment processes to improve efficiency and reduce costs. |

Let what.edu.vn be your trusted resource for all things eChecks. Ask your question today and get the answers you need to navigate the world of digital payments with confidence.