What Is Considered A Good Credit Score? If you’re asking that question, you’re on the right track to understanding your financial health. At WHAT.EDU.VN, we provide you with the information you need to understand credit scoring models like FICO and VantageScore, to help you achieve your financial goals. Creditworthiness, payment history and credit utilization are all vital aspects to consider.

1. Understanding Credit Scores: An Overview

A credit score is a numerical representation of your creditworthiness, based on your credit history. Lenders use this score to assess the risk of lending you money. A higher credit score generally indicates a lower risk, making you more likely to be approved for loans and credit cards with better terms. Both FICO and VantageScore are the two most commonly used credit scoring models. Understanding their ranges and how they evaluate your credit behavior is crucial for managing and improving your credit health.

2. FICO Score: What’s Considered Good?

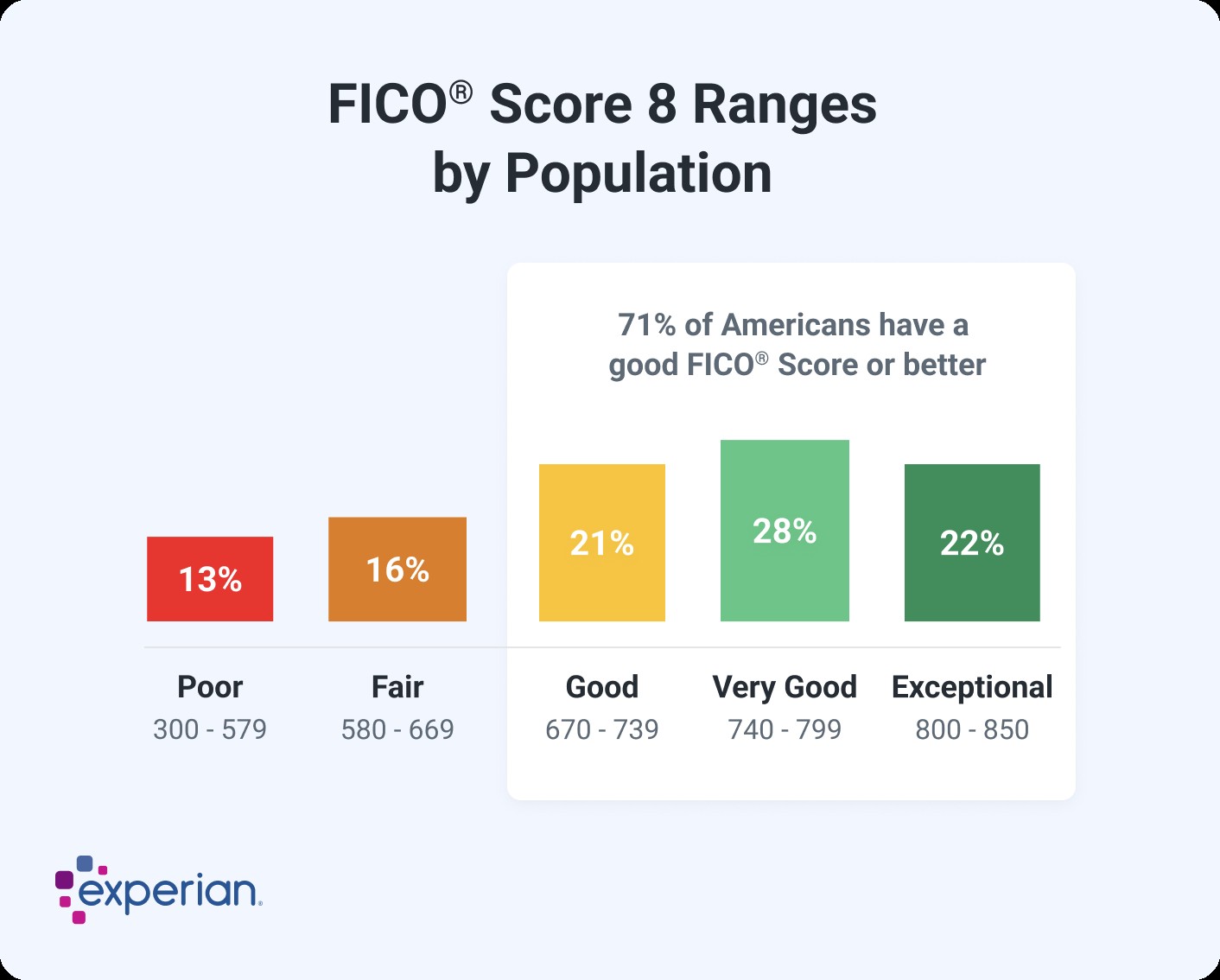

FICO (Fair Isaac Corporation) Score is widely used by lenders. The base FICO Scores range from 300 to 850, with different ranges indicating various levels of creditworthiness. Here’s a breakdown:

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Exceptional: 800-850

Generally, a FICO Score of 670 or higher is considered good. A score in the “Very Good” or “Exceptional” range will significantly improve your chances of getting approved for loans and credit cards with the best interest rates and terms. FICO also offers industry-specific scores (for auto loans and credit cards) with a range of 250-900, but the “Good” range remains the same, 670-739.

3. VantageScore: What’s Considered Good?

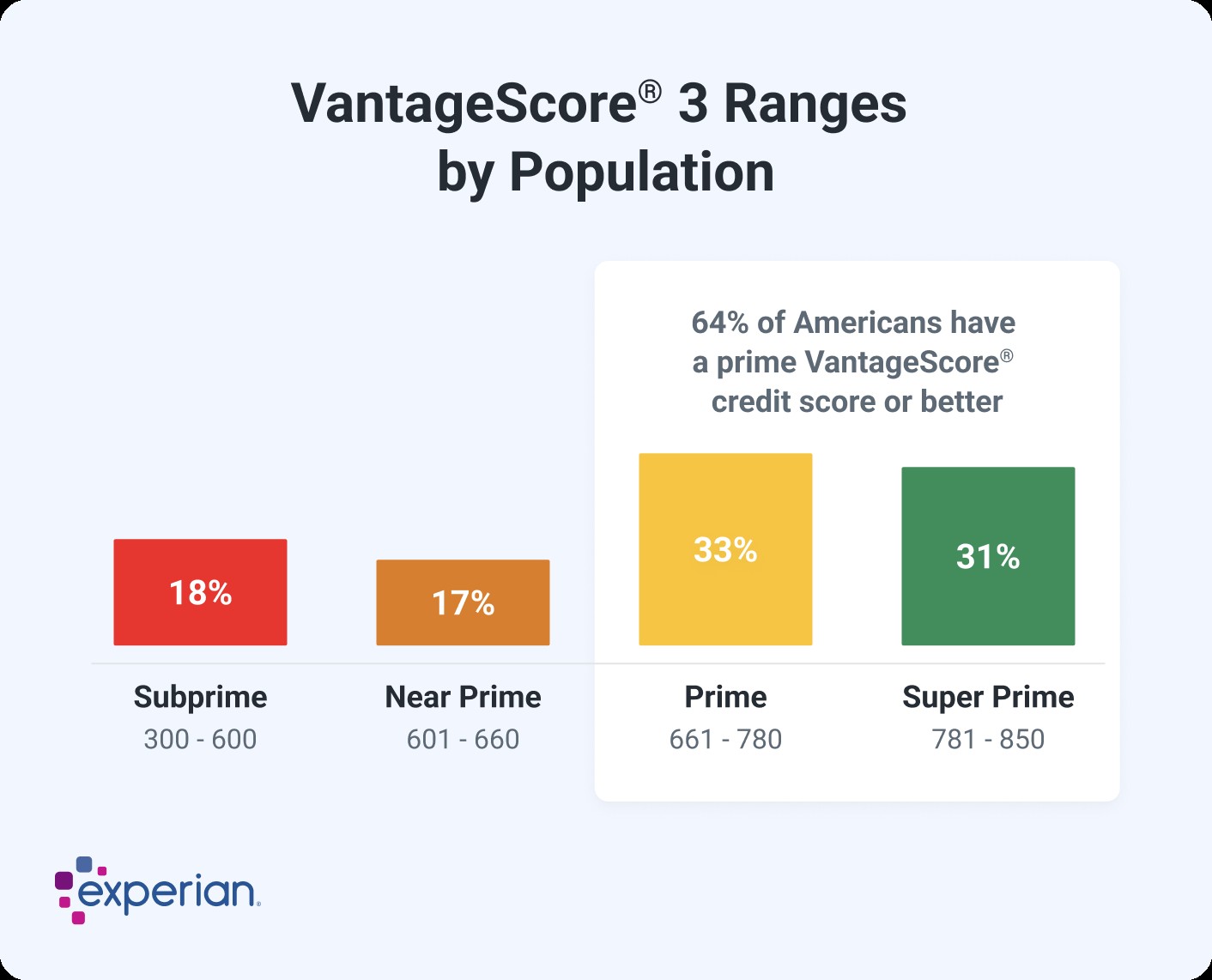

VantageScore is another popular credit scoring model, designed to be more inclusive and accessible. VantageScore 3.0 and 4.0, the latest versions, use the same 300-850 range as FICO. Here’s how VantageScore categorizes credit scores:

- Poor: 300-600

- Fair: 601-660

- Good: 661-780

- Excellent: 781-850

A VantageScore of 661 or higher is considered good. Achieving a score in the “Excellent” range can unlock the best financial opportunities. VantageScore aims to provide a more comprehensive view of your creditworthiness, considering factors like trended data (how your balances change over time).

4. Factors Affecting Your Credit Score

Understanding the factors that influence your credit score is essential for improving it. Both FICO and VantageScore consider similar factors, though they may weigh them differently. These factors include:

- Payment History: This is the most important factor. Paying your bills on time, every time, is crucial. Late payments can significantly lower your score.

- Amounts Owed: Also known as credit utilization, this refers to the amount of credit you’re using compared to your total available credit. Keeping your credit utilization low (below 30%) is important.

- Length of Credit History: A longer credit history generally leads to a higher score. The age of your oldest account, the age of your newest account, and the average age of all your accounts are considered.

- Credit Mix: Having a mix of different types of credit accounts (e.g., credit cards, installment loans, mortgages) can positively impact your score.

- New Credit: Opening too many new accounts in a short period can lower your score. Each new account results in a hard inquiry, which can slightly lower your score.

5. FICO Score Factors in Detail

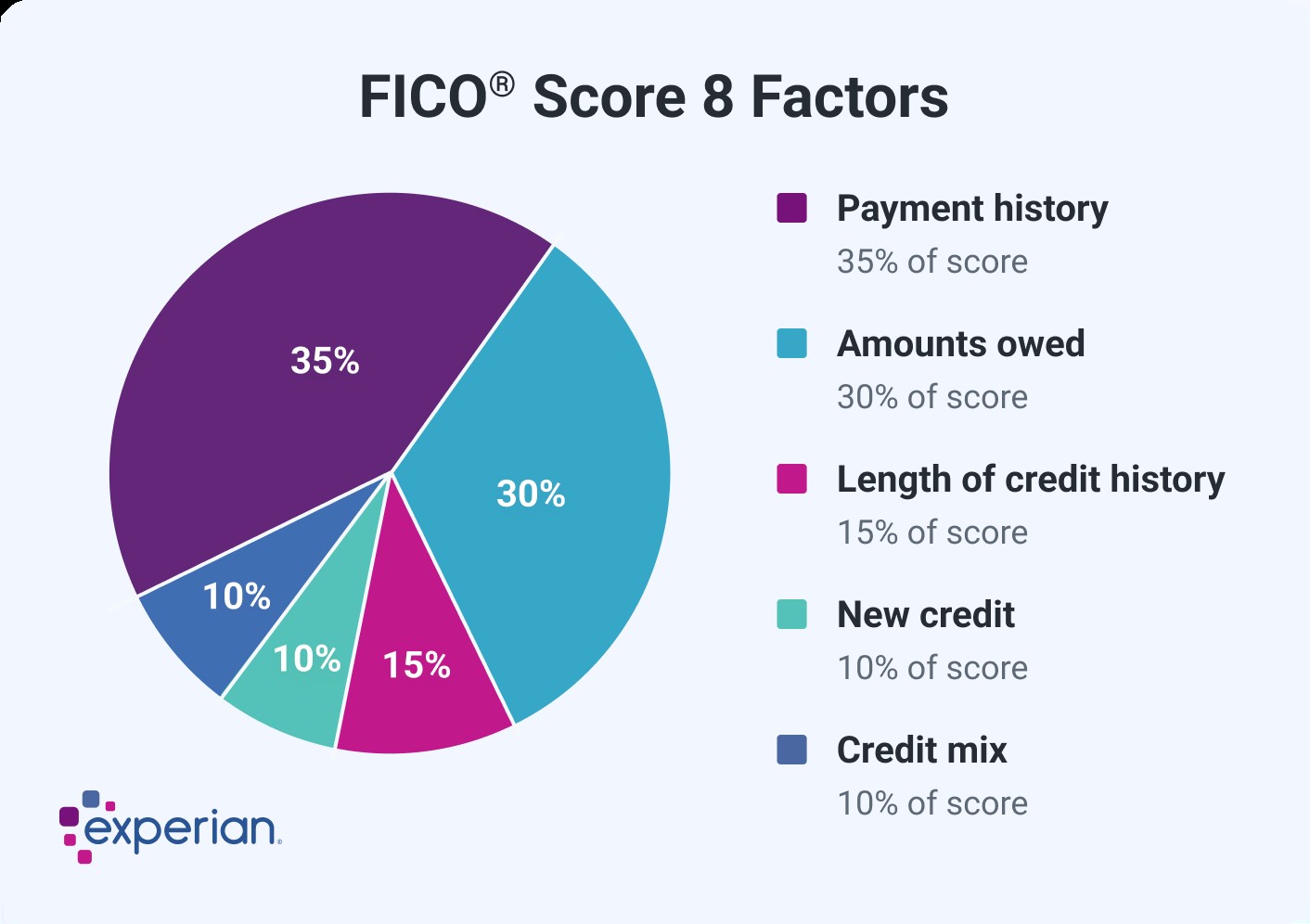

FICO uses percentages to represent the importance of each category. Keep in mind that the exact breakdown will depend on your individual credit report. Here’s a general overview:

- Payment History: 35%

- Amounts Owed: 30%

- Length of Credit History: 15%

- Credit Mix: 10%

- New Credit: 10%

6. VantageScore Factors in Detail

VantageScore lists the factors by how influential they are, rather than assigning specific percentages. The order of importance is:

| VantageScore Credit Scoring Factor | Importance |

|---|---|

| Payment history | Extremely influential |

| Total credit usage | Highly influential |

| Credit mix and experience | Highly influential |

| New accounts opened | Moderately influential |

| Balances and available credit | Less influential |

7. What Credit Scores Don’t Consider

It’s important to note that both FICO and VantageScore do not consider factors such as:

- Race

- Religion

- National origin

- Gender

- Marital status

- Income

- Employment history

- Where you live

These factors are legally protected and cannot be used in credit scoring.

8. Good Credit Score for Buying a House

A good credit score is essential when buying a house. It can increase your chances of approval for a mortgage and help you qualify for a lower interest rate. Generally, a FICO Score of at least 670 is recommended.

The minimum credit score needed to buy a house can range from 500 to 700, depending on the type of mortgage loan and the lender. For example, many lenders require a minimum credit score of 620 for a conventional mortgage. Government-backed mortgages, such as FHA, USDA, and VA loans, may have different requirements.

| Minimum Credit Score for Government-Backed Mortgages | Requirements |

|---|---|

| FHA home loans | 500-579 (10% down payment), 580+ (3.5% down payment) |

| USDA loans | 580-620 may be required by lenders, but there is no set minimum |

| VA loans | 620+ generally required by lenders |

Improving your credit score before applying for a mortgage can save you thousands of dollars in interest payments over the life of the loan.

9. Good Credit Score for Buying a Car

While there isn’t a specific minimum credit score required to buy a car, a VantageScore of 661 or higher is generally considered good. A higher credit score can help you qualify for better auto loan terms and lower interest rates.

Lenders view low credit scores as a sign of risk, so applicants with poor or fair credit will typically pay more in interest and might receive a lower loan limit. Improving your credit before buying a car can save you money on interest.

10. Why Different Credit Scores Exist

There are many different credit scores because credit scoring companies continually update and sell their scores to lenders. Lenders use credit scores to make decisions about lending and account management, such as who to approve and whether to change your credit limit.

FICO and VantageScore create and sell different credit scoring models, and both companies periodically release new versions of their scores. The latest scoring models might incorporate technological advances or changes in consumer behavior. Lenders can then decide to upgrade to a newer model or stick with the older version that’s already integrated into their systems and processes.

11. VantageScore’s Different Credit Scores Explained

VantageScore creates a generic tri-bureau scoring model, meaning the score is designed for any type of lender. The same model can evaluate your credit reports from the three major consumer credit bureaus (Experian, TransUnion, and Equifax).

VantageScore launched its first model in 2006. In 2017, it released VantageScore 4.0, which was the first generic credit score to use trended data, such as how your balances or credit utilization rate change over time. VantageScore announced its VantageScore 4plus™ model in May 2024, which allows creditors to ask consumers if they would like to link a bank account and share their banking data.

| VantageScore Credit Score Versions | Considers Data | Trended Data | Additional Data (with permission) |

|---|---|---|---|

| VS 3.0 | Credit Report | X | |

| VS 4.0 | Credit Report | X | |

| VS 4plus | Credit Report | X | Bank Account Data |

12. FICO’s Different Credit Scores Explained

In 1989, FICO became the first company to create credit scoring models based on consumer credit reports. Although recent FICO Score versions share a common name, such as FICO Score 8, FICO creates different versions of the models for each credit bureau.

There are three general types of consumer FICO Scores:

- Base FICO Scores: These scores are created for any type of lender and range from 300 to 850. The scores try to predict the likelihood that a consumer will fall behind on any type of credit obligation.

- Industry-specific FICO Scores: FICO creates auto scores and bankcard scores specifically for auto lenders and card issuers. Industry scores aim to predict the likelihood that a consumer will fall behind on the specific type of account, and the scores range from 250 to 900.

- FICO Scores that use alternative data: FICO has models that can incorporate alternative credit data, such as the UltraFICO and FICO XD scores. Both scores range from 300 to 850. The former can consider linking deposit account information, and the latter can score people using nontraditional types of payment history from other databases, such as your telecom or utility payments.

Creditors can choose which credit scores to use, and you often won’t know which report or score the lender will use.

13. Why Having a Good Credit Score Matters

Having good credit can make achieving your goals easier. It could be the difference between qualifying or being denied for an important loan, such as a home mortgage or car loan. It can also directly impact how much you’ll have to pay in interest or fees if you’re approved.

For example, the difference between taking out a 30-year, fixed-rate $350,000 mortgage with a 620 FICO Score and a 700 FICO Score could be significant. The lower score could mean higher monthly payments and tens of thousands of dollars in extra interest paid over the life of the loan.

Additionally, credit scores can impact non-lending decisions, such as whether a landlord will agree to rent you an apartment. Some employers may review your credit reports (but not your credit scores) before making a hiring or promotion decision. In most states, insurance companies may use credit-based insurance scores to help determine your premiums for auto, home, and life insurance.

| FICO Score | Interest Rate (30-Year Fixed-Rate Mortgage) | Monthly Payment | Total Interest Cost |

|---|---|---|---|

| 620 | 7.71% | $2,806.11 | $549,199 |

| 700 | 7.13% | $2,667.53 | $499,310 |

| 840 | 6.69% | $2,564.49 | $462,214 |

Source: Curinos LLC, December 6, 2024; assumes a $350,000 mortgage and 30-day rate-lock period.

14. How to Improve Your Credit Scores

To improve your credit scores, focus on the underlying factors that affect your scores. The basic steps you need to take are fairly straightforward:

- Pay your bills on time: This is the most important factor. Set up automatic payments or reminders to ensure you never miss a due date.

- Keep your credit utilization low: Aim to use no more than 30% of your available credit on each credit card.

- Check your credit reports for errors: Dispute any inaccuracies you find with the credit bureaus.

- Don’t open too many new accounts at once: Each new account can lower your score slightly.

- Maintain a mix of credit accounts: Having both credit cards and installment loans can benefit your score.

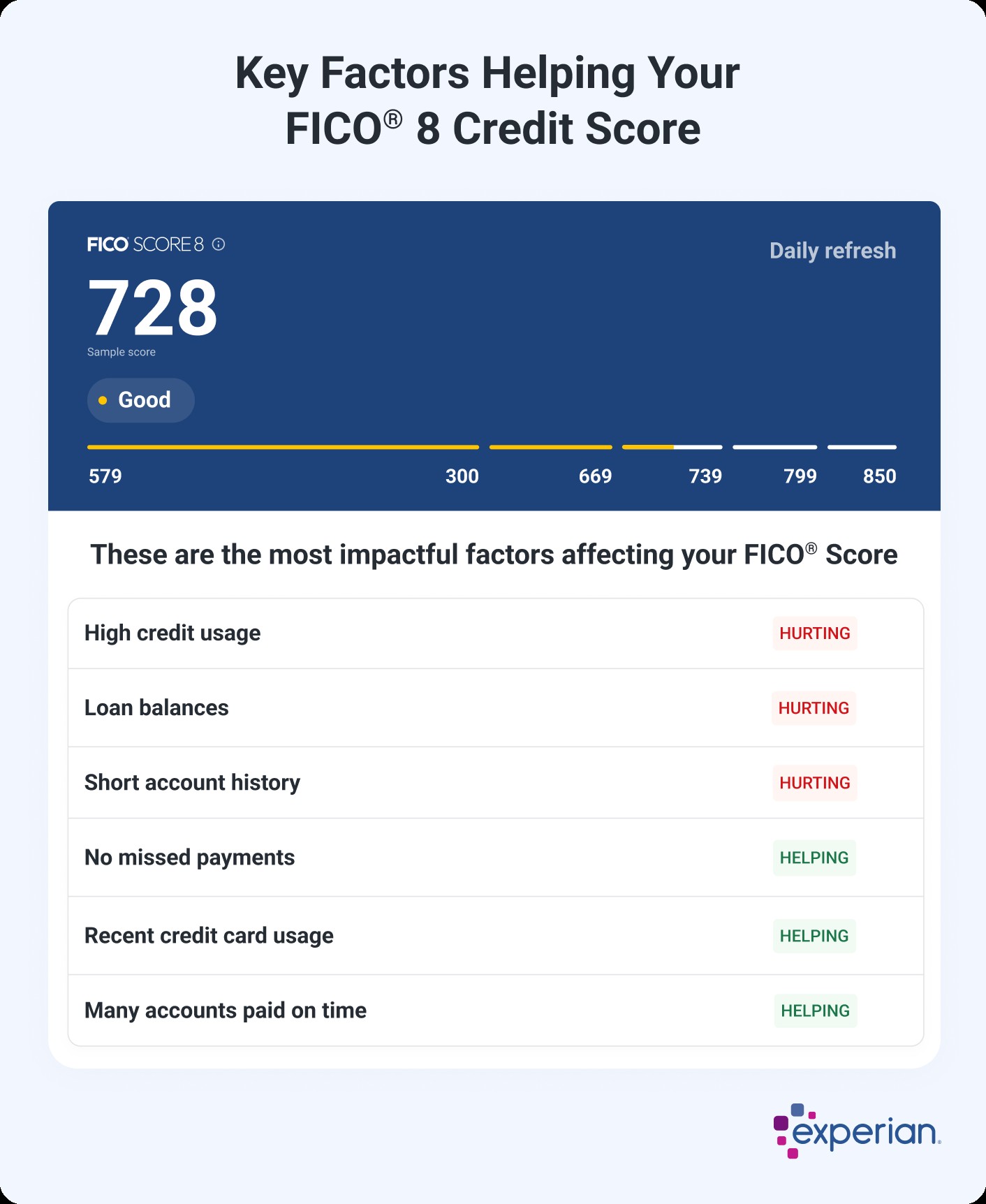

Other factors can also impact your scores. For example, increasing the average age of your accounts could help your scores. Checking your credit scores might also give you insight into what you can do to improve them.

You’ll also get an overview of your score profile, with an explanation of what’s helping and hurting your score the most.

15. What to Do if You Don’t Have a Credit Score

Credit scoring models can’t score credit reports that don’t have enough information. For FICO Scores, you need:

- An account that’s at least six months old

- An account that has been active in the past six months

VantageScore can score your credit report if it has at least one active account, even if the account is only a month old.

If you aren’t scoreable, you can:

- Become an authorized user: Ask a family member or friend with good credit to add you as an authorized user on their credit card.

- Apply for a secured credit card: These cards require a security deposit, which becomes your credit limit.

- Apply for a credit-builder loan: These loans are designed to help people with no credit history build credit.

- Report rent and utility payments: Some services can report your rent and utility payments to the credit bureaus.

16. Why Your Credit Score Changed

Your credit score can change for many reasons, and it’s not uncommon for scores to move up or down throughout the month as new information gets added to your credit reports.

Your credit scores might increase if:

- Negative items fall off your credit report

- You lower your credit utilization rate

- You pay off or settle collection accounts

- You add new on-time payments to your credit report

Your credit scores might decrease if:

- A credit card or loan payment becomes 30 days past due

- Your credit utilization rate increases

- You apply for or open a new credit account

- You file for bankruptcy

Some actions might have an unexpected impact on your credit scores. Paying off a loan, for example, could lead to a score drop even though it’s a positive action in terms of responsible money management.

17. Monitor Your Credit Report and Score Regularly

Checking your credit score right before you apply for a new loan or credit card can help you understand your chances of getting approved and qualifying for favorable terms. But regularly checking it further ahead of time gives you the chance to improve your scores and possibly save hundreds or thousands of dollars in interest.

18. Navigating Credit Scores with WHAT.EDU.VN

At WHAT.EDU.VN, we understand that navigating the world of credit scores can be daunting. That’s why we’re here to provide you with simple, straightforward answers to all your credit-related questions. Whether you’re wondering what constitutes a good credit score, how to improve your credit health, or what steps to take if you have no credit history, we’ve got you covered.

We offer a free platform where you can ask any question and receive prompt, accurate responses from experts in the field. We believe that everyone deserves access to clear, reliable information about credit, regardless of their background or financial situation.

19. Common Misconceptions About Credit Scores

There are several common misconceptions about credit scores that can lead to confusion and poor financial decisions. Here are a few to be aware of:

- Checking your own credit score will lower it: This is false. Checking your own credit score is considered a “soft inquiry” and does not affect your score.

- Closing credit card accounts will improve your score: This is not always the case. Closing accounts can reduce your available credit and increase your credit utilization, which can negatively impact your score.

- You need to carry a balance on your credit card to build credit: This is false. You can build credit by using your credit card and paying the balance in full each month.

- All credit scores are the same: This is false. Different credit scoring models exist, and lenders may use different models.

20. How to Leverage a Good Credit Score

Once you’ve achieved a good credit score, it’s important to leverage it to your advantage. Here are some ways to do that:

- Negotiate lower interest rates: Use your good credit score to negotiate lower interest rates on existing loans and credit cards.

- Refinance your mortgage: If you have a high interest rate on your mortgage, consider refinancing to a lower rate.

- Apply for rewards credit cards: A good credit score can help you qualify for credit cards with valuable rewards programs.

- Take advantage of better insurance rates: Insurance companies often offer lower rates to people with good credit scores.

21. Building and Maintaining Excellent Credit

Building and maintaining excellent credit is a long-term process that requires discipline and responsible financial habits. Here are some additional tips:

- Set up automatic payments: Automating your bill payments can help you avoid late payments and improve your payment history.

- Review your credit reports regularly: Checking your credit reports regularly can help you identify errors and potential fraud.

- Avoid maxing out your credit cards: Keeping your credit utilization low is crucial for maintaining a good credit score.

- Be patient: Building excellent credit takes time, so don’t get discouraged if you don’t see results immediately.

22. Credit Score Ranges and Financial Opportunities

Understanding how your credit score range impacts your financial opportunities can help you set goals and make informed decisions. Here’s a general overview:

- Poor (300-600): Limited access to credit, high interest rates, difficulty renting an apartment.

- Fair (601-660): Limited access to credit, higher interest rates, may require a co-signer for loans.

- Good (661-780): Good access to credit, average interest rates, able to rent an apartment and qualify for most loans.

- Excellent (781-850): Excellent access to credit, lowest interest rates, access to premium credit cards and financial products.

23. The Impact of Credit Inquiries

Credit inquiries occur when a lender checks your credit report to assess your creditworthiness. There are two types of credit inquiries:

- Soft inquiries: These occur when you check your own credit report or when a lender checks your credit report for pre-approval offers. Soft inquiries do not affect your credit score.

- Hard inquiries: These occur when you apply for a new credit card or loan. Hard inquiries can slightly lower your credit score.

It’s important to avoid applying for too many new accounts in a short period, as multiple hard inquiries can negatively impact your credit score.

24. Rebuilding Credit After Financial Setbacks

Financial setbacks, such as job loss or medical emergencies, can negatively impact your credit score. However, it’s possible to rebuild your credit after these setbacks. Here are some steps you can take:

- Create a budget: Develop a budget to help you manage your finances and prioritize debt repayment.

- Pay your bills on time: Make on-time payments your top priority to improve your payment history.

- Negotiate with creditors: Contact your creditors to negotiate payment plans or settlements.

- Consider credit counseling: A credit counselor can help you develop a plan to rebuild your credit.

25. Credit Scores and Identity Theft

Identity theft can have a devastating impact on your credit score. If you suspect you’ve been a victim of identity theft, take the following steps:

- Place a fraud alert on your credit reports: This will require lenders to verify your identity before opening new accounts in your name.

- Review your credit reports for unauthorized activity: Dispute any unauthorized accounts or transactions.

- File a police report: This can help you document the identity theft and protect yourself from liability.

- Contact the Federal Trade Commission (FTC): The FTC can provide you with resources and guidance on how to recover from identity theft.

26. The Future of Credit Scoring

The credit scoring landscape is constantly evolving. New technologies and data sources are being used to develop more accurate and comprehensive credit scoring models. Some trends to watch include:

- Alternative data: The use of alternative data, such as rent and utility payments, to score people with limited credit histories.

- AI and machine learning: The use of AI and machine learning to develop more sophisticated credit scoring models.

- Open banking: The use of open banking data to assess creditworthiness based on banking transaction history.

27. Understanding Credit Reports

Your credit report is a detailed record of your credit history. It contains information about your credit accounts, payment history, and any negative items, such as bankruptcies or collections. It’s important to review your credit reports regularly to ensure they are accurate and to identify any potential fraud.

You are entitled to one free credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) each year. You can request your free credit reports at AnnualCreditReport.com.

28. Credit Scores vs. Credit Reports

It’s important to understand the difference between credit scores and credit reports. Your credit score is a numerical representation of your creditworthiness, while your credit report is a detailed record of your credit history. Your credit score is based on the information in your credit report.

Lenders use both your credit score and your credit report to assess your creditworthiness. Your credit score provides a quick snapshot of your credit health, while your credit report provides more detailed information about your credit history.

29. Credit Score Monitoring Services

Credit score monitoring services can help you stay informed about your credit health. These services typically provide you with:

- Regular credit score updates: You’ll receive regular updates on your credit score, so you can track your progress over time.

- Credit report monitoring: You’ll receive alerts when changes are made to your credit report, such as new accounts or negative items.

- Identity theft protection: Some services offer identity theft protection features, such as fraud alerts and credit freezes.

30. Seeking Professional Credit Advice

If you’re struggling to understand or improve your credit score, it may be helpful to seek professional credit advice. Credit counselors can provide you with personalized guidance and support to help you achieve your credit goals.

Credit counselors can help you:

- Review your credit reports and scores: They can help you understand your credit history and identify areas for improvement.

- Develop a budget and debt management plan: They can help you create a budget and develop a plan to repay your debts.

- Negotiate with creditors: They can help you negotiate payment plans or settlements with your creditors.

- Provide education on credit-related topics: They can educate you on credit scoring, credit reports, and other credit-related topics.

31. The Role of Credit Unions in Building Credit

Credit unions are member-owned financial institutions that often offer more favorable terms and rates than traditional banks. They can be a great resource for building credit, especially if you have limited credit history.

Credit unions may offer:

- Secured credit cards: These cards can help you build credit even if you have no credit history or poor credit.

- Credit-builder loans: These loans are designed to help people with limited credit history build credit.

- Personalized financial advice: Credit union staff can provide you with personalized financial advice and support.

32. The Importance of Financial Literacy

Financial literacy is the ability to understand and effectively use financial skills, including personal financial management, budgeting, and investing. Improving your financial literacy can help you make informed decisions about your finances and build a strong financial foundation.

Resources for improving your financial literacy include:

- Online courses: Many websites offer free or low-cost online courses on financial literacy topics.

- Workshops and seminars: Community organizations and financial institutions often offer workshops and seminars on financial literacy.

- Books and articles: Numerous books and articles are available on financial literacy topics.

- Financial advisors: Financial advisors can provide you with personalized guidance and support to help you achieve your financial goals.

33. Maintaining a Healthy Credit Profile Through Economic Downturns

Economic downturns can present challenges to maintaining a healthy credit profile. Job loss, reduced income, and increased expenses can make it difficult to pay your bills on time. Here are some tips for maintaining a healthy credit profile during economic downturns:

- Prioritize essential bills: Focus on paying essential bills, such as rent, mortgage, utilities, and food.

- Contact creditors: If you’re struggling to pay your bills, contact your creditors to discuss payment options.

- Avoid taking on new debt: Avoid taking on new debt unless it’s absolutely necessary.

- Review your budget: Review your budget regularly to identify areas where you can cut expenses.

- Seek assistance: Contact government agencies or non-profit organizations for assistance with food, housing, or other essential needs.

34. Credit Scores and Small Business Loans

If you’re a small business owner, your personal credit score can play a significant role in your ability to obtain a small business loan. Lenders often review your personal credit score to assess your creditworthiness and determine whether to approve your loan application.

Maintaining a good personal credit score can increase your chances of getting approved for a small business loan and help you qualify for better terms and rates.

35. The Impact of Divorce on Credit Scores

Divorce can have a significant impact on your credit score. Joint credit accounts, such as credit cards and mortgages, can become a source of conflict and financial stress during a divorce.

To protect your credit score during a divorce:

- Close joint credit accounts: Close joint credit accounts as soon as possible to prevent your ex-spouse from incurring debt that you’ll be responsible for.

- Remove yourself as an authorized user: If you’re an authorized user on your ex-spouse’s credit card, remove yourself from the account.

- Monitor your credit reports: Monitor your credit reports regularly to ensure that your ex-spouse is not opening new accounts in your name or failing to pay joint debts.

- Consult with a financial advisor: A financial advisor can help you navigate the financial challenges of divorce and protect your credit score.

36. Credit Scores and Insurance Premiums

In most states, insurance companies use credit-based insurance scores to help determine your premiums for auto, home, and life insurance. Credit-based insurance scores are based on the information in your credit report and are used to predict the likelihood that you’ll file a claim.

Maintaining a good credit score can help you qualify for lower insurance premiums.

37. Understanding Credit Score Volatility

Credit scores can fluctuate over time due to a variety of factors. Understanding the reasons for credit score volatility can help you manage your credit health and avoid surprises.

Factors that can cause credit score volatility include:

- Changes in your credit utilization: Increasing your credit utilization can lower your score, while decreasing it can raise your score.

- Late payments: Late payments can significantly lower your score.

- New credit accounts: Opening too many new credit accounts in a short period can lower your score.

- Closing credit accounts: Closing credit accounts can lower your score if it reduces your available credit or negatively impacts your credit mix.

- Negative items: Negative items, such as bankruptcies or collections, can significantly lower your score.

38. The Convenience of WHAT.EDU.VN

At WHAT.EDU.VN, we understand that you need answers quickly. That’s why we offer a convenient platform where you can ask any question and receive prompt, accurate responses. Whether you’re struggling to understand a complex financial concept or simply need a quick answer to a credit-related question, we’re here to help.

Our services are completely free, so you can ask as many questions as you like without worrying about the cost. We believe that everyone deserves access to reliable financial information, regardless of their background or income level.

Have questions about credit scores? Don’t hesitate to reach out to us at WHAT.EDU.VN. Our team of experts is ready to provide you with the answers you need.

Contact us:

Address: 888 Question City Plaza, Seattle, WA 98101, United States

Whatsapp: +1 (206) 555-7890

Website: WHAT.EDU.VN

Let what.edu.vn be your trusted resource for all things credit-related. Ask your question today and get the clarity you deserve.