What Is Excellent Credit? It’s a question many ask, and at WHAT.EDU.VN, we’re here to provide clarity. An excellent credit score unlocks better financial opportunities, from lower interest rates to easier loan approvals. Discover how to attain credit excellence and maintain a stellar credit rating. We’ll explore good credit standing, credit health, and financial well-being throughout this comprehensive guide.

1. Defining Excellent Credit: What Does It Mean?

Excellent credit isn’t just a number; it’s a gateway to financial opportunities. A high credit score signifies trustworthiness to lenders, opening doors to better interest rates and favorable loan terms. Let’s explore what constitutes excellent credit and why it matters.

1.1. Understanding Credit Score Ranges

Credit scores typically range from 300 to 850. While different scoring models exist, the general principle remains the same: the higher the score, the better your creditworthiness.

- Poor Credit: 300-579

- Fair Credit: 580-669

- Good Credit: 670-739

- Very Good Credit: 740-799

- Excellent Credit: 800-850

1.2. What Constitutes an Excellent Credit Score?

An “excellent” credit score generally falls within the 800-850 range. This signifies a borrower with a history of responsible credit management, making them a low-risk candidate for lenders.

1.3. The Significance of an Excellent Credit Score

Having an excellent credit score is more than just a badge of honor; it translates to tangible financial benefits. These include:

- Lower Interest Rates: Access to the lowest interest rates on loans and credit cards.

- Higher Approval Odds: Increased likelihood of approval for credit applications.

- Better Loan Terms: Favorable loan terms, such as lower down payments and longer repayment periods.

- Premium Rewards: Eligibility for premium credit cards with lucrative rewards programs.

- Increased Financial Flexibility: Greater financial flexibility and opportunities.

2. FICO® Score: The Gold Standard

FICO® Scores are widely used by lenders to assess credit risk. Understanding how FICO® Scores work is crucial for achieving and maintaining excellent credit.

2.1. FICO® Score Ranges

FICO® Scores range from 300 to 850, with higher scores indicating lower credit risk.

2.2. What Is Considered a Good FICO® Score?

A FICO® Score of 670 to 739 is generally considered good, while a score of 740 to 799 is considered very good. An excellent FICO® Score falls within the 800-850 range.

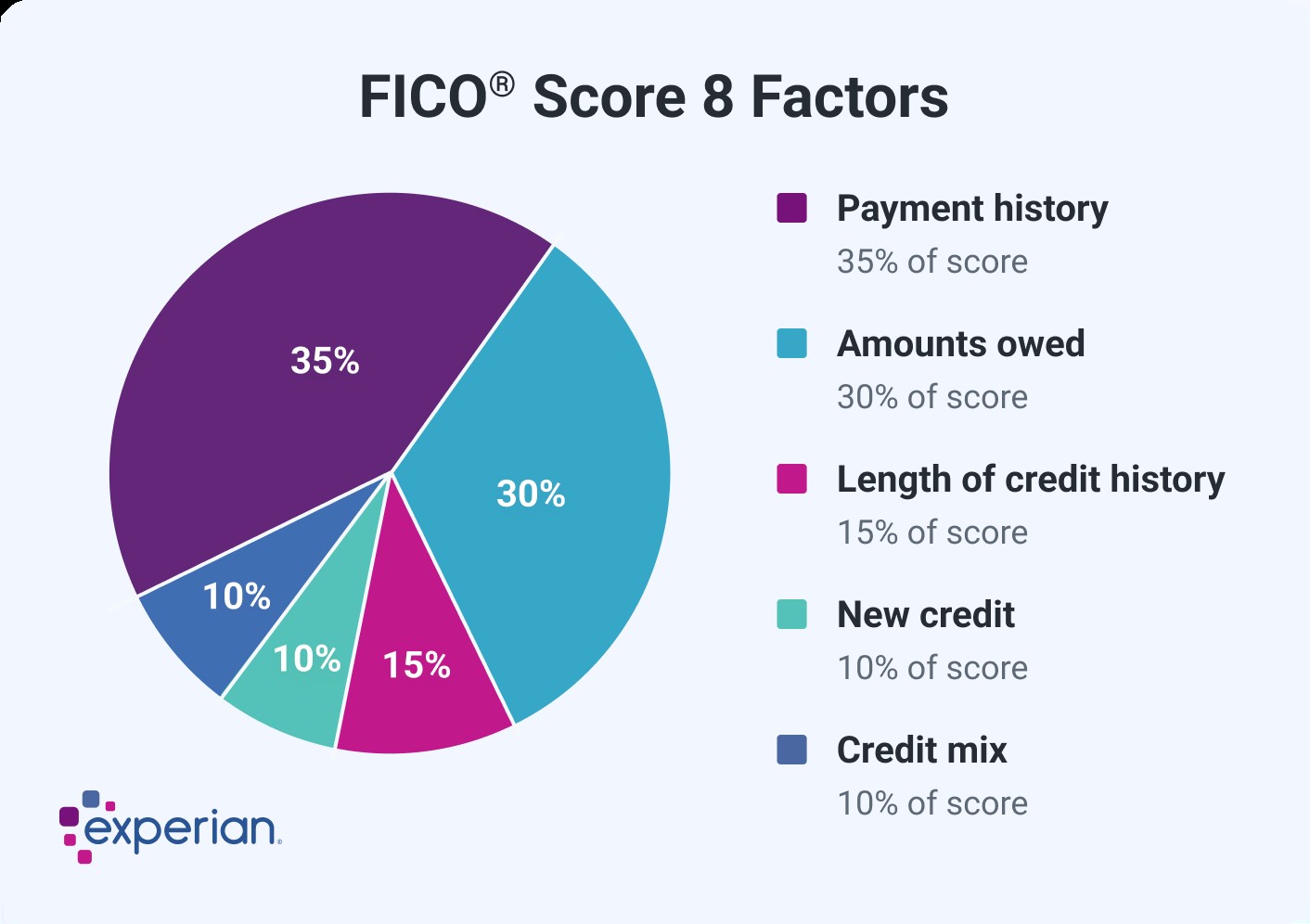

2.3. Factors Influencing FICO® Scores

FICO® Scores are calculated based on several factors, each weighted differently:

- Payment History (35%): The most significant factor, reflecting your track record of on-time payments.

- Amounts Owed (30%): The amount of debt you owe relative to your available credit.

- Length of Credit History (15%): The age of your credit accounts.

- Credit Mix (10%): The variety of credit accounts you have (e.g., credit cards, loans).

- New Credit (10%): Recent credit applications and new accounts.

2.4. FICO® Score Versions

FICO® offers various versions of its scoring models, including base FICO® Scores and industry-specific scores. Lenders may use different versions, so it’s essential to monitor your scores regularly.

3. VantageScore®: An Alternative Credit Scoring Model

VantageScore® is another widely used credit scoring model. Understanding VantageScore® can provide a more comprehensive view of your creditworthiness.

3.1. VantageScore® Ranges

VantageScore® also uses a scoring range of 300 to 850, similar to FICO®.

3.2. What Is Considered a Good VantageScore®?

A VantageScore® of 661 to 780 is generally considered good. Scores above 781 are considered excellent.

3.3. Factors Influencing VantageScore®

VantageScore® considers similar factors as FICO®, but with slightly different weightings:

- Payment History: Extremely influential

- Total Credit Usage: Highly influential

- Credit Mix and Experience: Highly influential

- New Accounts Opened: Moderately influential

- Balances and Available Credit: Less influential

3.4. VantageScore® Versions

VantageScore® has released updated models over the years. The latest versions incorporate trended data and alternative data sources.

| VantageScore Credit Scoring Factor | Importance |

|---|---|

| Payment history | Extremely influential |

| Total credit usage | Highly influential |

| Credit mix and experience | Highly influential |

| New accounts opened | Moderately influential |

| Balances and available credit | Less influential |

4. Benefits of Having Excellent Credit

Excellent credit offers a multitude of financial advantages that can significantly impact your life.

4.1. Access to Lower Interest Rates

One of the most significant benefits of excellent credit is access to lower interest rates on loans and credit cards. This can save you thousands of dollars over the life of a loan.

4.2. Higher Approval Odds for Loans and Credit Cards

With excellent credit, you’re more likely to be approved for loans and credit cards, even those with strict eligibility requirements.

4.3. Favorable Loan Terms

Lenders offer more favorable loan terms to borrowers with excellent credit, such as lower down payments and longer repayment periods.

4.4. Premium Rewards and Perks

Excellent credit can qualify you for premium credit cards with lucrative rewards programs, travel perks, and other valuable benefits.

4.5. Increased Financial Flexibility

Excellent credit provides greater financial flexibility and opportunities, allowing you to pursue your goals with confidence.

5. How to Achieve Excellent Credit

Building excellent credit takes time and discipline, but the rewards are well worth the effort.

5.1. Pay Bills on Time, Every Time

Payment history is the most critical factor in your credit score. Make sure to pay all bills on time, every time.

5.2. Keep Credit Utilization Low

Credit utilization is the amount of credit you’re using relative to your available credit. Aim to keep your credit utilization below 30%.

5.3. Monitor Your Credit Reports Regularly

Regularly monitoring your credit reports allows you to identify and correct any errors that could be affecting your credit score.

5.4. Avoid Opening Too Many New Accounts

Opening too many new accounts in a short period can lower your credit score. Be selective and only apply for credit when you need it.

5.5. Maintain a Mix of Credit Accounts

Having a mix of credit accounts, such as credit cards and loans, can demonstrate responsible credit management.

6. Maintaining Excellent Credit

Once you’ve achieved excellent credit, it’s essential to maintain it through responsible financial habits.

6.1. Continue Paying Bills on Time

Consistency is key to maintaining excellent credit. Continue paying all bills on time, every time.

6.2. Keep Credit Utilization Low

Continue to keep your credit utilization low by paying down balances and avoiding excessive spending.

6.3. Monitor Your Credit Reports Regularly

Regularly monitor your credit reports to detect and address any potential issues.

6.4. Avoid Closing Old Credit Accounts

Closing old credit accounts can shorten your credit history and lower your credit score. Keep them open if possible, even if you don’t use them.

6.5. Be Mindful of New Credit Applications

Be mindful of new credit applications and avoid applying for too much credit at once.

7. Credit Scores and Major Life Decisions

Your credit score plays a significant role in major life decisions, such as buying a house or a car.

7.1. Buying a House

A good credit score is essential for qualifying for a mortgage with a low interest rate.

7.2. Buying a Car

A good credit score can help you secure a car loan with favorable terms.

7.3. Renting an Apartment

Landlords often check credit scores as part of the rental application process.

7.4. Getting Insurance

Insurance companies may use credit scores to determine premiums for auto, home, and life insurance.

7.5. Employment

Some employers may review credit reports as part of the hiring process.

8. Common Myths About Credit Scores

There are many misconceptions about credit scores. Let’s debunk some common myths.

8.1. Checking Your Own Credit Score Will Lower It

Checking your own credit score does not lower it. Only hard inquiries, such as those from lenders, can affect your score.

8.2. Closing Credit Card Accounts Will Improve Your Score

Closing credit card accounts can lower your score, especially if they’re old or have high credit limits.

8.3. Carrying a Balance on Your Credit Card Is Good for Your Score

Carrying a balance on your credit card is not good for your score. It increases your credit utilization and can lead to interest charges.

8.4. Income Affects Your Credit Score

Income does not directly affect your credit score. However, it can indirectly affect your ability to pay bills on time.

8.5. All Credit Scores Are the Same

There are many different credit scoring models, and each may use slightly different factors to calculate your score.

9. Understanding Credit Reports

Credit reports are detailed records of your credit history. Understanding how to read and interpret your credit reports is crucial for maintaining excellent credit.

9.1. What Information Is Included in a Credit Report?

Credit reports include information such as:

- Personal information (name, address, Social Security number)

- Credit accounts (credit cards, loans)

- Payment history

- Credit inquiries

- Public records (bankruptcies, liens)

9.2. How to Obtain Your Credit Reports

You’re entitled to a free credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax) every 12 months.

9.3. How to Dispute Errors on Your Credit Reports

If you find errors on your credit reports, you have the right to dispute them with the credit bureaus.

9.4. The Importance of Monitoring Your Credit Reports

Regularly monitoring your credit reports allows you to identify and correct any errors that could be affecting your credit score.

10. How to Improve a Fair or Good Credit Score

If you don’t have excellent credit yet, there are steps you can take to improve your score.

10.1. Make Payments on Time

The most important step is to make all payments on time, every time.

10.2. Reduce Credit Card Debt

Reducing your credit card debt can lower your credit utilization and improve your score.

10.3. Become an Authorized User

Becoming an authorized user on someone else’s credit card can help you build credit.

10.4. Consider a Secured Credit Card

A secured credit card requires a security deposit and can be a good option for building credit if you have limited or no credit history.

10.5. Use a Credit-Builder Loan

A credit-builder loan is a small loan designed to help you build credit.

11. Credit Repair Services: Are They Worth It?

Credit repair services claim to help you improve your credit score by disputing errors on your credit reports. However, it’s essential to be cautious when considering these services.

11.1. What Credit Repair Services Do

Credit repair services typically offer to:

- Obtain your credit reports

- Identify errors on your credit reports

- Dispute errors with the credit bureaus

- Negotiate with creditors

11.2. The Risks of Using Credit Repair Services

There are several risks associated with using credit repair services:

- They may charge high fees

- They may make false or misleading claims

- They cannot guarantee results

- You can do everything they do yourself for free

11.3. Alternatives to Credit Repair Services

Instead of using credit repair services, consider these alternatives:

- Obtain your credit reports yourself

- Dispute errors with the credit bureaus yourself

- Negotiate with creditors yourself

- Seek advice from a non-profit credit counseling agency

12. Credit Counseling: A Helpful Resource

Credit counseling agencies can provide valuable assistance with managing debt and improving your credit score.

12.1. What Credit Counseling Agencies Do

Credit counseling agencies typically offer services such as:

- Debt management plans

- Budget counseling

- Credit counseling

- Education on financial topics

12.2. How to Find a Reputable Credit Counseling Agency

When choosing a credit counseling agency, look for one that is:

- Non-profit

- Accredited

- Offers a range of services

- Has experienced counselors

12.3. The Benefits of Credit Counseling

Credit counseling can help you:

- Manage debt

- Improve your credit score

- Develop a budget

- Learn about financial topics

13. Building Credit with Limited or No Credit History

If you have limited or no credit history, there are steps you can take to build credit.

13.1. Become an Authorized User

Becoming an authorized user on someone else’s credit card can help you build credit.

13.2. Consider a Secured Credit Card

A secured credit card requires a security deposit and can be a good option for building credit.

13.3. Use a Credit-Builder Loan

A credit-builder loan is a small loan designed to help you build credit.

13.4. Report Rent and Utility Payments

Some credit bureaus allow you to report rent and utility payments, which can help you build credit.

13.5. Apply for a Student Loan

Student loans can help you build credit, but be sure to make payments on time.

14. The Impact of Late Payments on Your Credit Score

Late payments can have a significant negative impact on your credit score.

14.1. How Late Payments Affect Your Credit Score

Late payments can lower your credit score, especially if they’re recent or frequent.

14.2. How Long Late Payments Stay on Your Credit Report

Late payments can stay on your credit report for up to seven years.

14.3. How to Minimize the Impact of Late Payments

If you’ve made a late payment, take these steps to minimize the impact:

- Contact the creditor and explain the situation

- Make the payment as soon as possible

- Set up automatic payments to avoid future late payments

15. How Bankruptcy Affects Your Credit Score

Bankruptcy can have a severe negative impact on your credit score.

15.1. The Impact of Bankruptcy on Your Credit Score

Bankruptcy can significantly lower your credit score and make it difficult to obtain credit in the future.

15.2. How Long Bankruptcy Stays on Your Credit Report

Bankruptcy can stay on your credit report for up to 10 years.

15.3. How to Rebuild Credit After Bankruptcy

Rebuilding credit after bankruptcy takes time and effort. Here are some steps you can take:

- Obtain a secured credit card

- Make all payments on time

- Avoid taking on too much debt

- Monitor your credit reports regularly

16. Credit Score Monitoring Services

Credit score monitoring services can help you track your credit score and receive alerts about changes to your credit report.

16.1. What Credit Score Monitoring Services Do

Credit score monitoring services typically offer features such as:

- Daily or monthly credit score updates

- Credit report monitoring

- Alerts about changes to your credit report

- Identity theft protection

16.2. The Benefits of Using a Credit Score Monitoring Service

Credit score monitoring services can help you:

- Track your credit score over time

- Detect errors on your credit report

- Identify potential fraud

- Receive alerts about important changes to your credit report

16.3. How to Choose a Credit Score Monitoring Service

When choosing a credit score monitoring service, consider factors such as:

- Cost

- Features

- Reputation

- Customer service

17. Identity Theft and Credit Scores

Identity theft can have a devastating impact on your credit score.

17.1. How Identity Theft Affects Your Credit Score

Identity theft can result in fraudulent accounts, unauthorized charges, and other negative information being added to your credit report.

17.2. Steps to Take if You’re a Victim of Identity Theft

If you’re a victim of identity theft, take these steps:

- Contact the credit bureaus and place a fraud alert on your credit reports

- File a police report

- Contact your creditors and close any fraudulent accounts

- Monitor your credit reports regularly

17.3. How to Prevent Identity Theft

Here are some tips for preventing identity theft:

- Protect your Social Security number

- Shred documents containing personal information

- Be cautious of phishing scams

- Monitor your credit reports regularly

18. The Future of Credit Scoring

The credit scoring landscape is constantly evolving.

18.1. Emerging Trends in Credit Scoring

Emerging trends in credit scoring include:

- The use of alternative data sources

- The incorporation of trended data

- The development of more sophisticated scoring models

18.2. How Technology Is Changing Credit Scoring

Technology is playing an increasingly important role in credit scoring, with the development of new tools and techniques for assessing credit risk.

18.3. The Impact of These Changes on Consumers

These changes could make it easier for consumers to access credit and improve their credit scores.

19. Frequently Asked Questions (FAQs) About Excellent Credit

Let’s address some frequently asked questions about excellent credit.

| Question | Answer |

|---|---|

| What is the highest credit score possible? | The highest credit score possible is 850. |

| How long does it take to build excellent credit? | It can take several years to build excellent credit, depending on your starting point and credit habits. |

| What is the difference between a FICO® Score and a VantageScore®? | FICO® Score and VantageScore® are both widely used credit scoring models, but they use slightly different factors to calculate your score. |

| How often should I check my credit score? | You should check your credit score regularly, at least once a year. |

| Can I get a loan with bad credit? | It’s possible to get a loan with bad credit, but you’ll likely pay a higher interest rate. |

| What is a good credit utilization ratio? | A good credit utilization ratio is below 30%. |

| How do I dispute errors on my credit report? | You can dispute errors on your credit report by contacting the credit bureaus and providing documentation to support your claim. |

| Can I remove negative items from my credit report? | You can only remove negative items from your credit report if they are inaccurate or unverifiable. |

| What is a secured credit card? | A secured credit card requires a security deposit and can be a good option for building credit if you have limited or no credit history. |

| How does closing a credit card account affect my credit score? | Closing a credit card account can lower your credit score, especially if it’s an old account or has a high credit limit. |

20. Expert Tips for Maintaining Excellent Credit

Here are some expert tips for maintaining excellent credit:

- Pay your bills on time, every time: Set up automatic payments to avoid late payments.

- Keep your credit utilization low: Aim to keep your credit utilization below 30%.

- Monitor your credit reports regularly: Check your credit reports for errors and signs of fraud.

- Avoid opening too many new accounts: Be selective and only apply for credit when you need it.

- Maintain a mix of credit accounts: Having a mix of credit cards and loans can demonstrate responsible credit management.

- Be patient: Building and maintaining excellent credit takes time and discipline.

21. Resources for Learning More About Credit

Here are some valuable resources for learning more about credit:

- WHAT.EDU.VN: Your go-to source for answering any question about credit, for free.

- Experian: Offers credit reports, credit scores, and credit education resources.

- TransUnion: Provides credit reports, credit scores, and credit monitoring services.

- Equifax: Offers credit reports, credit scores, and identity theft protection services.

- The Consumer Financial Protection Bureau (CFPB): A government agency that provides consumer education and protection.

- The Federal Trade Commission (FTC): A government agency that enforces consumer protection laws.

22. The Importance of Financial Literacy

Financial literacy is essential for making informed financial decisions and achieving financial well-being.

22.1. What Is Financial Literacy?

Financial literacy is the ability to understand and effectively use various financial skills, including:

- Budgeting

- Saving

- Investing

- Debt management

- Credit management

22.2. Why Financial Literacy Matters

Financial literacy empowers you to:

- Make informed financial decisions

- Achieve your financial goals

- Avoid financial pitfalls

- Build wealth

- Improve your overall well-being

22.3. How to Improve Your Financial Literacy

Here are some ways to improve your financial literacy:

- Read books and articles about personal finance

- Take online courses or attend workshops

- Seek advice from a financial advisor

- Use budgeting apps and tools

- Monitor your finances regularly

23. Credit and Debt Management Strategies

Effective credit and debt management strategies are essential for maintaining excellent credit.

23.1. Budgeting Techniques

Budgeting is the foundation of sound financial management. Here are some budgeting techniques:

- The 50/30/20 Rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

- Zero-Based Budgeting: Allocate every dollar of your income to a specific purpose.

- Envelope Budgeting: Use cash for discretionary spending and allocate it to different envelopes.

23.2. Debt Repayment Strategies

Here are some effective debt repayment strategies:

- The Debt Snowball Method: Pay off the smallest debts first to gain momentum.

- The Debt Avalanche Method: Pay off the debts with the highest interest rates first to save money.

- Debt Consolidation: Combine multiple debts into a single loan with a lower interest rate.

23.3. Negotiating with Creditors

You may be able to negotiate with creditors to:

- Lower your interest rate

- Waive late fees

- Set up a payment plan

24. Building a Strong Credit Foundation for the Future

Building a strong credit foundation early in life can set you up for financial success.

24.1. Starting Early with Credit

The earlier you start building credit, the better.

24.2. Teaching Children About Credit

Teach children about the importance of credit and responsible financial habits.

24.3. Setting Financial Goals

Set financial goals and develop a plan to achieve them.

25. Success Stories: Achieving and Maintaining Excellent Credit

Let’s look at some success stories of people who have achieved and maintained excellent credit.

25.1. From Bad Credit to Excellent Credit

Share a story of someone who turned their credit around from bad to excellent.

25.2. Maintaining Excellent Credit Through Life’s Challenges

Share a story of someone who maintained excellent credit through challenging life events.

25.3. The Benefits of Excellent Credit in Real Life

Share a story of someone who benefited from excellent credit in a tangible way.

26. Credit and Relationships

Credit can play a significant role in relationships.

26.1. Talking to Your Partner About Credit

Openly discuss credit and finances with your partner.

26.2. Joint Credit Accounts

Understand the risks and benefits of joint credit accounts.

26.3. How Credit Can Impact Relationships

Credit issues can strain relationships, so it’s essential to address them proactively.

27. Protecting Your Credit During Economic Downturns

Economic downturns can pose challenges to your credit.

27.1. Staying Proactive with Your Finances

Stay proactive with your finances and monitor your credit regularly.

27.2. Communicating with Creditors

Communicate with creditors if you’re facing financial difficulties.

27.3. Seeking Financial Assistance

Seek financial assistance from government programs or non-profit organizations if needed.

28. Credit for Small Business Owners

Credit is essential for small business owners.

28.1. Building Business Credit

Build business credit separately from personal credit.

28.2. Using Credit to Grow Your Business

Use credit strategically to grow your business.

28.3. Managing Business Debt

Manage business debt responsibly.

29. Credit and Retirement Planning

Credit can impact your retirement planning.

29.1. Paying Off Debt Before Retirement

Aim to pay off debt before retirement.

29.2. Using Credit Wisely in Retirement

Use credit wisely in retirement and avoid taking on unnecessary debt.

29.3. Protecting Your Credit in Retirement

Protect your credit in retirement by monitoring your credit reports and avoiding scams.

30. Conclusion: Embrace the Power of Excellent Credit

Excellent credit is a valuable asset that can unlock financial opportunities and improve your overall well-being. By understanding the factors that influence your credit score and adopting responsible financial habits, you can achieve and maintain excellent credit and embrace the power it holds. At WHAT.EDU.VN, we’re committed to helping you answer any question and navigate the world of credit with confidence.

If you have any questions about credit scores or need personalized advice, don’t hesitate to reach out to us at WHAT.EDU.VN. We offer free consultations and are here to help you achieve your financial goals. Contact us at 888 Question City Plaza, Seattle, WA 98101, United States. Whatsapp: +1 (206) 555-7890 or visit our website WHAT.EDU.VN to ask your questions and receive answers for free. We’re here to assist you every step of the way toward your financial success. Don’t wait – ask your question today.

Experiencing difficulties in finding reliable answers to your questions? Unsure where to turn for trustworthy advice without incurring costs? Visit what.edu.vn today and ask your question to connect with our community of experts who are ready to help you find the solutions you need. Unlock the power of knowledge and take control of your learning journey now.