For credit scores ranging from 300 to 850, a score in the mid to high 600s is generally considered good. Scores in the high 700s and 800s are considered excellent. In fact, around a third of consumers have FICO® Scores between 600 and 750, and an impressive 48% score even higher. The average FICO® Score in the U.S. in 2023 was 715, highlighting that a “good” credit score is indeed achievable for many.

Lenders use credit scores as a key factor in deciding who they will lend to and at what interest rates. A higher credit score generally translates to better financial opportunities, helping you qualify for credit cards and loans with lower interest rates and more favorable terms. While there are different types of credit scores, primarily FICO® Score and VantageScore®, they share similar scoring factors and ranges.

Let’s delve deeper into what constitutes a good credit score, explore the factors that influence your credit, and discuss how you can improve your scores.

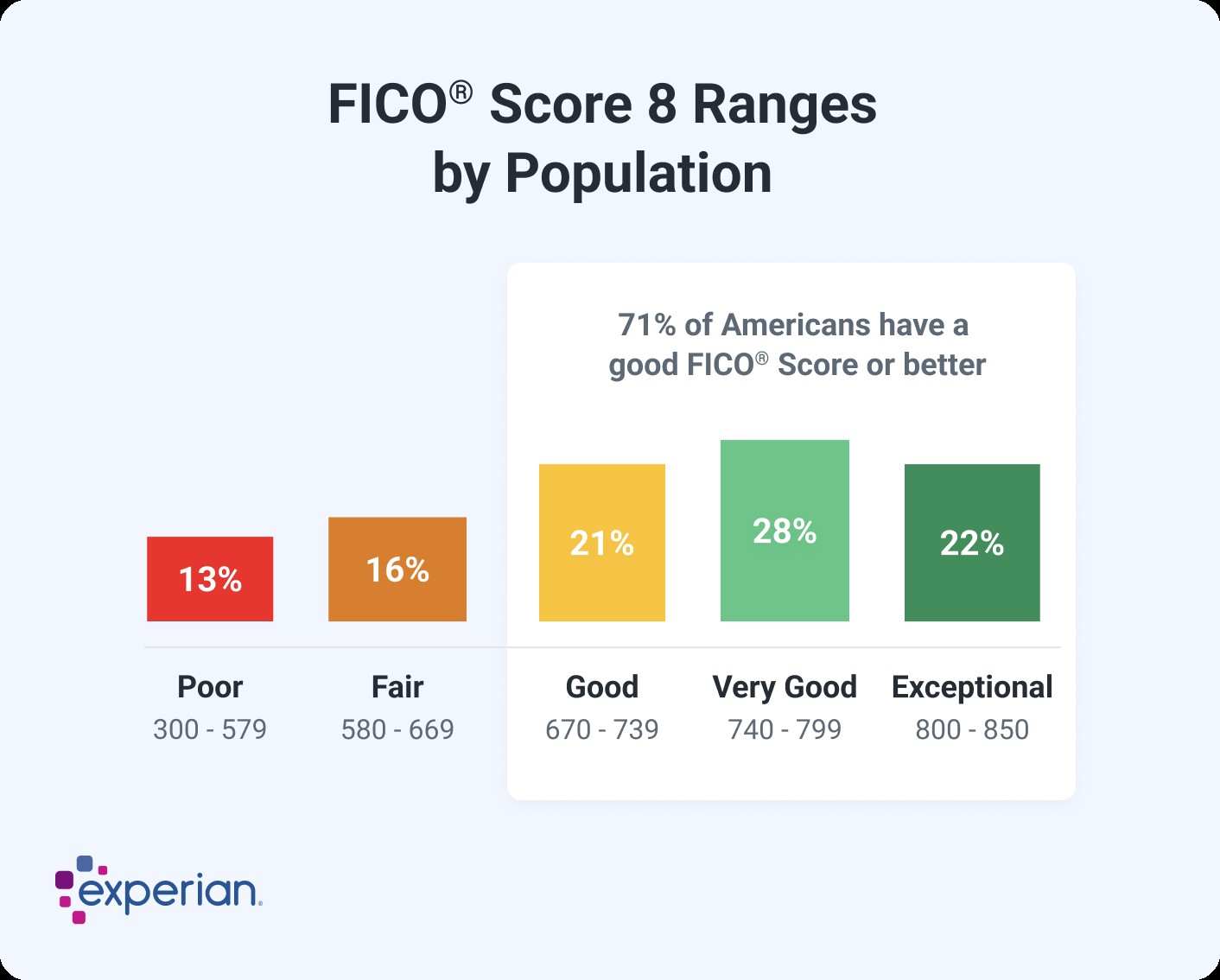

Decoding Good FICO® Scores

The base FICO® Scores operate on a scale of 300 to 850. Within this range, a good FICO® Score falls between 670 and 739.

FICO®, a leading credit scoring agency, develops various types of consumer credit scores. They offer “base” FICO® Scores for general lending purposes across industries, as well as industry-specific scores tailored for credit card issuers and auto lenders. Interestingly, FICO’s industry-specific credit scores have a slightly different range, from 250 to 900. However, the “good” range remains consistent: 670 to 739 for industry-specific FICO® Scores as well. Scores exceeding this range are categorized as very good or exceptional, reflecting even lower risk for lenders.

Further Reading: What Is the Average Credit Score in the US?

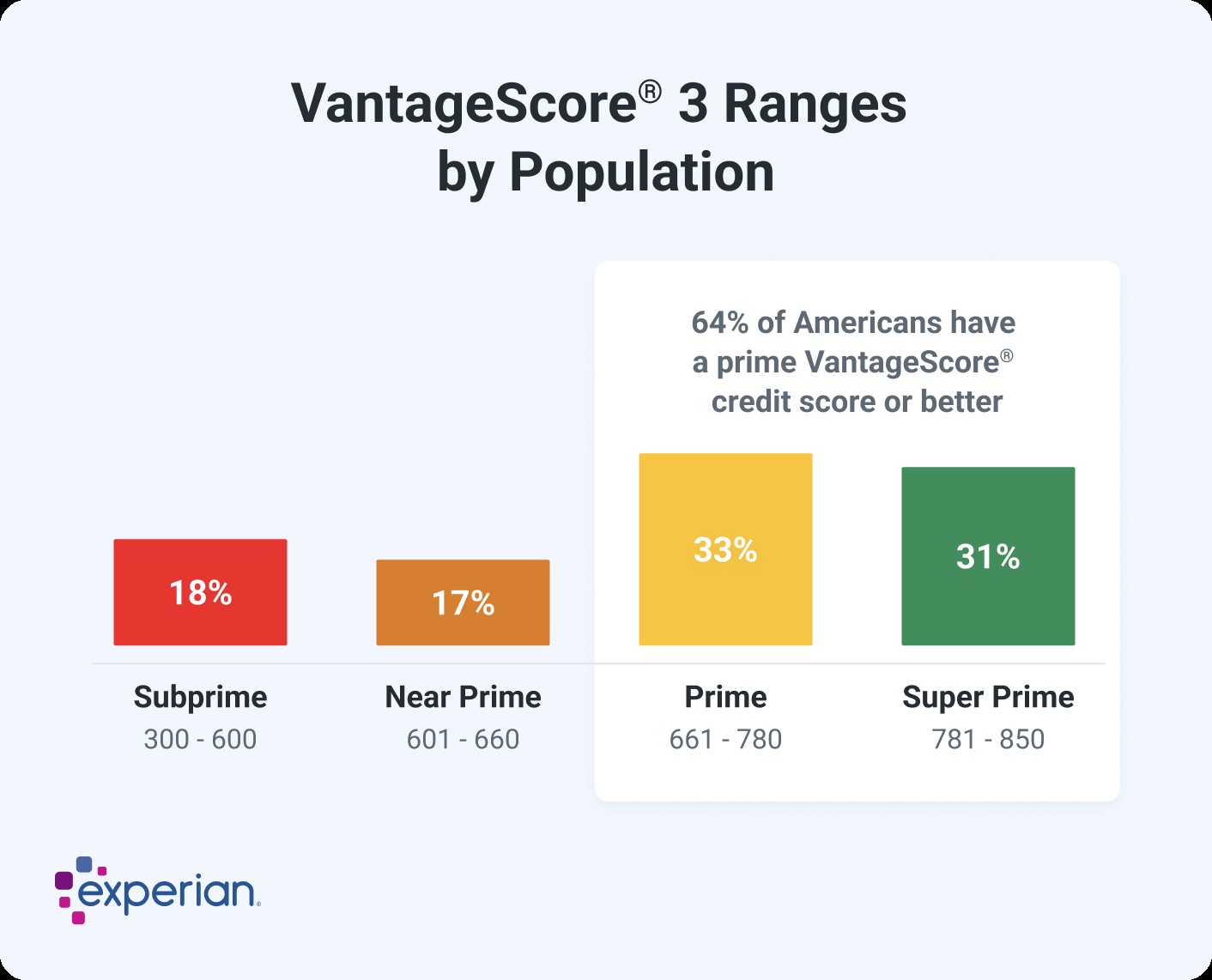

Understanding Good VantageScore Credit Scores

VantageScore 3.0 and 4.0, the latest models, also utilize a 300 to 850 range, mirroring the base FICO® Scores. For VantageScore, a good credit score ranges from 661 to 780.

VantageScore, another prominent credit scoring model, distinguishes itself by not offering industry-specific scores. However, they have consistently updated their models over the years. While earlier VantageScore versions (1.0 and 2.0) had a 501 to 990 range, these are not commonly used by lenders today.

Key Factors Influencing Your Credit Scores

Several common factors play a significant role in determining your credit scores, regardless of whether it’s a FICO® Score or VantageScore. These factors generally fall into categories such as payment history, amounts owed, credit history length, credit mix, and new credit.

While both FICO® and VantageScore consider these categories, they weigh their importance differently.

Learn More: What Affects Your Credit Scores?

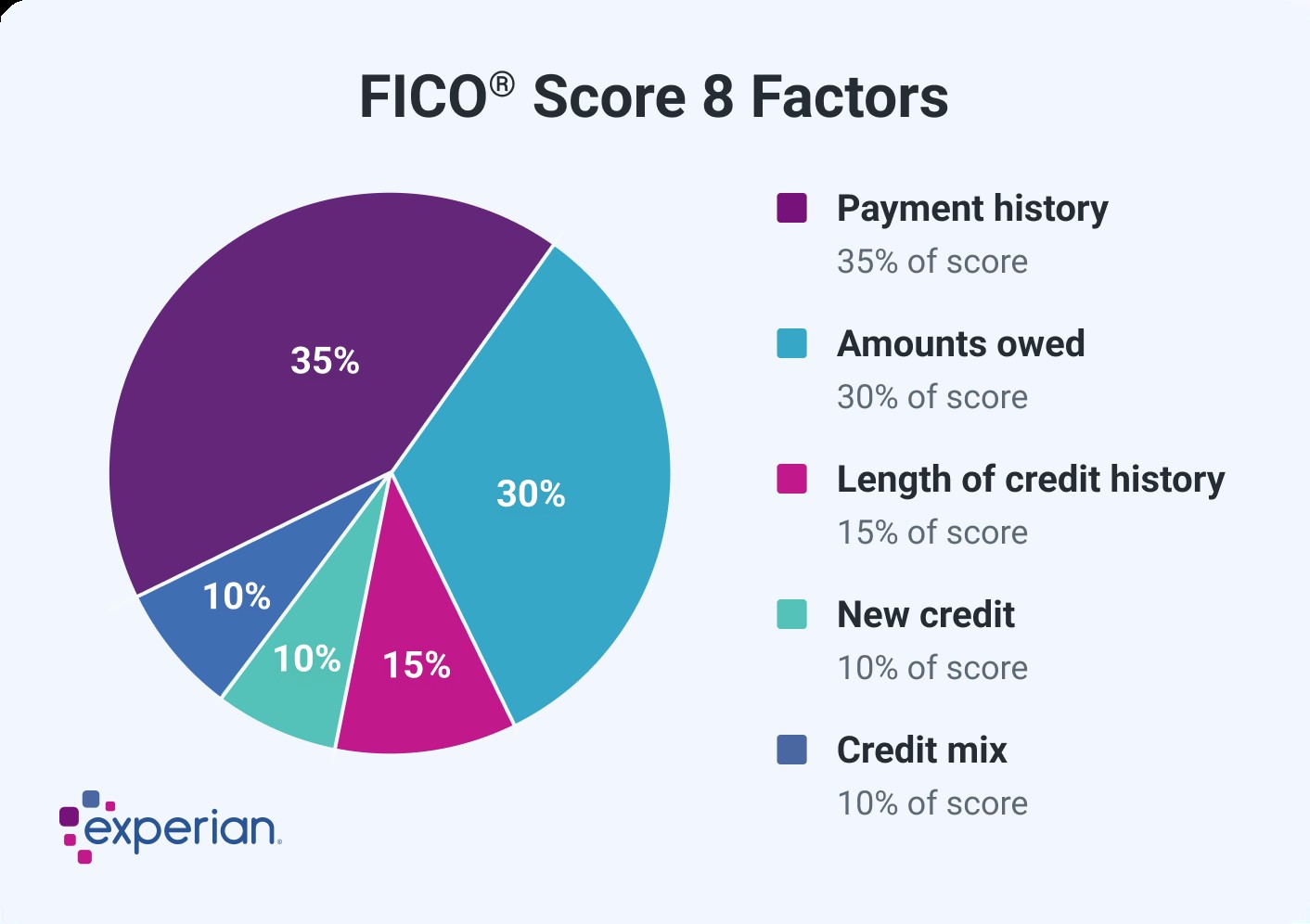

FICO® Score Factors: A Deeper Dive

FICO® uses percentages to indicate the general importance of each category. However, it’s crucial to remember that the precise percentage breakdown for your individual score is based on your unique credit report. The weight of these scoring factors according to FICO® is generally as follows:

VantageScore Credit Score Factors: Understanding Influence Levels

VantageScore ranks factors by their general influence on credit scores, acknowledging that individual credit reports vary. The influence levels for VantageScore factors are:

| VantageScore Credit Scoring Factor | Importance |

|---|---|

| Payment history | Extremely influential |

| Total credit usage | Highly influential |

| Credit mix and experience | Highly influential |

| New accounts opened | Moderately influential |

| Balances and available credit | Less influential |

Information Not Considered in Credit Scores

It’s important to note that both FICO® and VantageScore do not consider certain types of information when calculating your credit scores. This includes factors like your race, religion, national origin, marital status, age, salary, occupation, employer, and where you live. Credit scores are solely based on your credit history and how you manage credit.

What’s a Good Credit Score for Buying a House?

Aiming for a good credit score or higher is essential when buying a house to increase your approval odds and secure a lower mortgage interest rate. For FICO® Scores, this means targeting at least 670.

While the minimum credit score to buy a house can vary from around 500 to 700, it depends on the type of mortgage loan and the lender. Many lenders require a minimum credit score of 620 for a conventional mortgage. Government-backed mortgages have different minimum credit score requirements:

| Minimum Credit Score for Government-Backed Mortgages |

|---|

| FHA home loans |

| USDA loans |

| VA loans |

Remember, a better credit score often translates to a lower interest rate on your mortgage, saving you significant money over the loan’s lifetime. While getting a mortgage with bad credit might be possible, improving your score before applying for a mortgage is highly recommended.

Further Reading: Which Credit Scores Do Mortgage Lenders Use?

What’s Considered a Good Credit Score for Buying a Car?

While there isn’t a specific minimum credit score to buy a car, a VantageScore of 661 or higher is generally considered good for auto loans. As with mortgages, a higher credit score can unlock better auto loan terms.

Auto lenders perceive lower credit scores as higher risk, leading to higher interest rates and potentially lower loan amounts for applicants with fair or poor credit. If your score isn’t in the good range, it’s wise to focus on improving your credit before you buy a car.

Further Reading: Average Car Loan Interest Rates by Credit Score

Why Are There Different Credit Scores?

The existence of multiple credit scores stems from the fact that credit scoring companies are constantly refining and selling their scoring models to lenders.

Lenders rely on credit scores for various lending decisions, including loan approvals and credit limit adjustments. They have the flexibility to choose which scoring model they prefer to use.

FICO® and VantageScore® are the primary creators and sellers of credit scoring models. Both companies regularly release updated versions, incorporating technological advancements and shifts in consumer behavior. Lenders can then opt to upgrade to newer models or stick with older versions already integrated into their systems.

Further Reading: Why Are My Credit Scores Different?

VantageScore’s Range of Credit Scores

VantageScore focuses on a generic tri-bureau scoring model, designed for use by any type of lender. This single model can analyze credit reports from all three major credit bureaus: Experian, TransUnion, and Equifax.

VantageScore’s journey began with VantageScore 1.0 in 2006 (no longer offered). In 2017, they launched VantageScore 4.0, the first generic credit score to incorporate trended data, analyzing balance and credit utilization changes over time.

More recently, VantageScore announced VantageScore 4plus™ in May 2024. This model allows creditors to request consumer permission to link a bank account and share banking data. With permission, VantageScore 4plus™ can consider this banking data to recalculate scores.

| Recent VantageScore Credit Score Versions | VantageScore 3.0 | VantageScore 4.0 | VantageScore 4plus |

|---|---|---|---|

| Only considers data from a credit report | X | X | |

| Can consider additional data with permission | X | ||

| Considers trended data | X | X |

FICO®’s Diverse Credit Score Versions

FICO® pioneered credit scoring based on consumer credit reports in 1989. While recent FICO® Score versions share names like FICO® Score 8, FICO® develops distinct versions for each credit bureau.

FICO® offers three main types of consumer scores:

- Base FICO® Scores: Designed for all lender types, ranging from 300 to 850. They predict the likelihood of falling behind on any credit obligation.

- Industry-specific FICO® Scores: Tailored for auto lenders and card issuers, with a range of 250 to 900. These scores predict the likelihood of falling behind on specific account types (auto loans or credit cards).

- FICO® Scores using alternative data: Including UltraFICO® and FICO® XD, ranging from 300 to 850. UltraFICO® can incorporate deposit account information, while FICO® XD scores individuals using non-traditional payment history (telecom, utility payments) from other databases.

FICO® industry-specific scores build upon a base FICO® Score. FICO® regularly releases new score suites, like the FICO® Score 10 Suite, which includes base FICO® Score 10, FICO® Score 10 T (with trended data), and industry-specific scores.

Lender Choice in Credit Score Usage

Lenders decide which credit reports to request and which credit scores to obtain. You often won’t know their specific choices, and lender preferences can change.

Fortunately, most FICO® and VantageScore® credit scores utilize similar underlying information from your credit reports. They share the same goal: predicting the likelihood of becoming 90 days past due on a bill within 24 months.

Consequently, the same factors impact all your credit scores. While scores may vary across models and credit reports, they generally move in the same direction over time.

The Importance of Having a Good Credit Score

A good credit score significantly facilitates achieving your financial goals. It can be the deciding factor in loan approvals, especially for major purchases like homes or cars. It also directly influences interest rates and fees.

For instance, consider a $350,000, 30-year fixed-rate mortgage. The difference between a 620 and 700 FICO® Score could be $138.58 per month. Over the loan’s duration, a better score could save you $49,889 in interest.

Beyond lending, credit scores impact non-lending decisions, such as apartment rentals.

Your credit reports can also be reviewed by employers (not scores) for hiring or promotion decisions and by insurance companies in most states to determine premiums using credit-based insurance scores.

| Average Mortgage Rates Based on FICO® Score | |||

|---|---|---|---|

| FICO® Score | Interest Rate, 30-Year Fixed-Rate Mortgage | Monthly Payment | Total Interest Cost |

| 620 | 7.71% | $2,806.11 | $549,199 |

| 700 | 7.13% | $2,667.53 | $499,310 |

| 840 | 6.69% | $2,564.49 | $462,214 |

Source: Curinos LLC, December 6, 2024; assumes a $350,000 mortgage and 30-day rate-lock period

Further Reading: Facts About Credit You May Not Know

Strategies to Improve Your Credit Scores

To improve your credit scores, focus on the core factors that influence them. The fundamental steps are straightforward:

- Pay bills on time: Consistent on-time payments are crucial.

- Lower credit utilization: Keep your credit card balances low compared to your credit limits.

- Become an authorized user: Piggyback on someone else’s responsible credit use.

- Apply for a secured credit card: A good option for building or rebuilding credit.

- Limit new credit applications: Avoid opening too many accounts at once.

Other factors, like increasing the average age of your accounts, can also help, but often involve time rather than direct action.

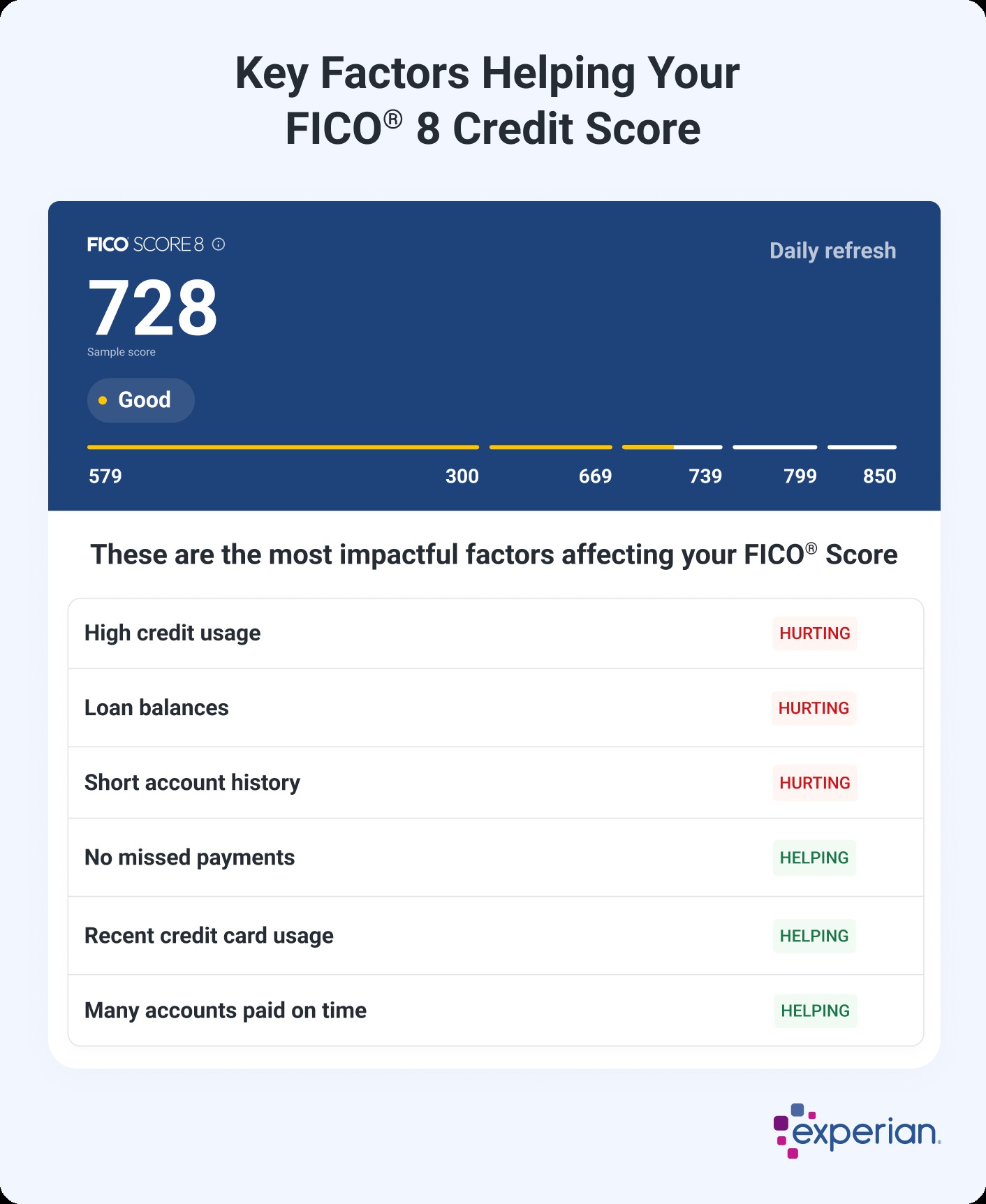

Regularly checking your credit scores provides insights into areas for improvement. For example, your free Experian FICO® Score 8 comes with an overview of how lenders view your credit:

You’ll also receive a score profile, explaining factors positively and negatively impacting your score.

What to Do if You Don’t Have a Credit Score

Credit scoring models cannot generate scores without sufficient credit history.

For FICO® Scores, you need:

- An account at least six months old.

- Account activity within the past six months.

VantageScore can score reports with at least one active account, even if only a month old.

If you are unscorable, you can:

- Become an authorized user.

- Apply for a secured credit card.

- Consider credit-builder loans.

Further Reading: Ways to Build Credit if You Have No Credit History

Why Your Credit Score Might Have Changed

Credit scores fluctuate for various reasons, often changing monthly as new information updates your credit reports.

Scores may increase](/blogs/ask-experian/why-did-my-credit-score-go-up/) if:

- Negative items are removed from your report.

- Credit utilization decreases.

- Collection accounts are paid off.

- New on-time payments are added.

Conversely, scores may decrease](/blogs/ask-experian/why-did-my-credit-score-drop/) if:

- Payments become 30 days late.

- Credit utilization increases.

- New credit accounts are opened.

- Bankruptcy is filed.

Unexpectedly, paying off a loan could temporarily lower your score, especially if it was your only installment loan. This can shift your credit mix negatively.

Credit scoring models use complex calculations; a single event’s point impact depends on your overall credit profile. A late payment might drastically impact someone with a pristine history, while having less impact on someone with existing late payments.

Regularly Monitor Your Credit Report and Score

Checking your credit score before applying for new credit is beneficial, but regular monitoring provides the opportunity to improve your scores proactively, potentially saving you money on interest.

You can check and monitor your Experian FICO® Score and credit report for free with daily updates and real-time alerts. Free accounts also offer credit-building tools like Experian Boost and personalized credit insights.