Are you curious about what underwriting in insurance entails? WHAT.EDU.VN provides clear and concise answers to your pressing questions, offering insights into insurance risk assessment and more. Discover how insurers evaluate risk and determine policy pricing with our comprehensive guide. Explore insurance assessment, risk evaluation, and insurance analysis for free.

1. Understanding Insurance Underwriting: The Basics

Insurance underwriting is the critical process insurance companies use to evaluate the risk of insuring a potential client. It’s about deciding whether to offer insurance, and if so, at what price. This involves a detailed review of the applicant’s information to assess the level of risk they represent. Think of it as the gatekeeper ensuring the insurance company makes sound financial decisions by accurately pricing risk.

2. The Importance of Underwriting for Insurers

Underwriting is essential for insurance companies to maintain financial stability. Effective underwriting ensures the company collects enough in premiums to cover claims and operational costs, while also remaining profitable. Poor underwriting can lead to significant financial losses.

3. The Underwriting Process: A Step-by-Step Guide

The underwriting process involves several key steps:

3.1. Application Submission

The process starts when a potential client submits an insurance application. This application includes detailed information about the applicant, the assets to be insured, and the type of coverage sought.

3.2. Information Gathering

The underwriter reviews the application to determine if they have enough information to accurately assess the risk. They may request additional information from the applicant or third parties. This could include medical records, financial statements, or inspection reports.

3.3. Risk Assessment

Once all the necessary information is gathered, the underwriter evaluates the risk. This involves analyzing the applicant’s history, current circumstances, and potential future risks.

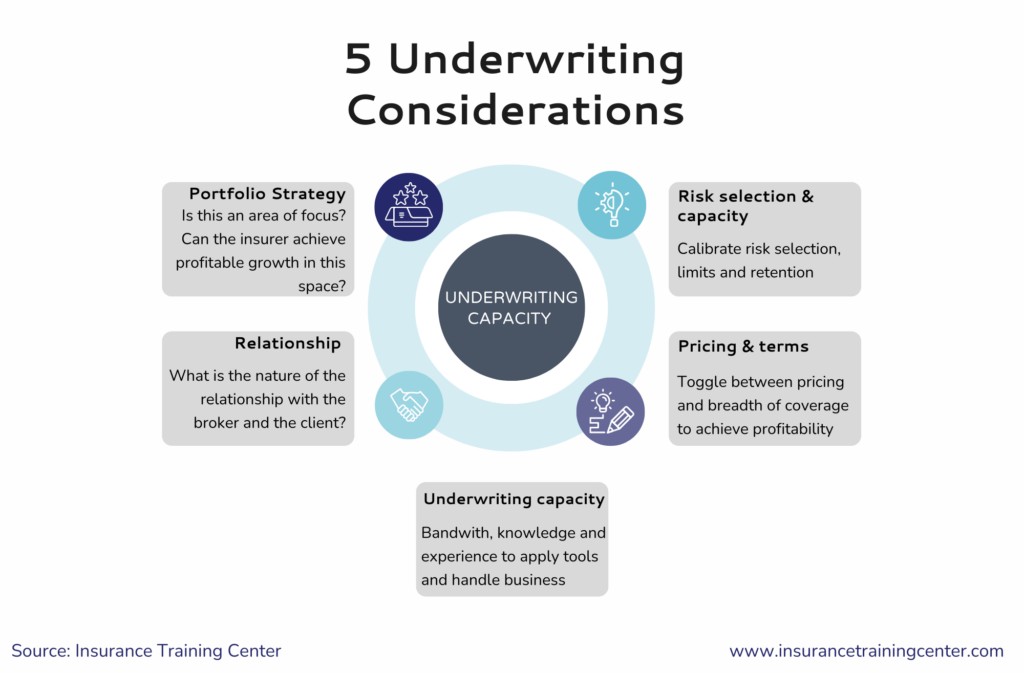

3.4. Pricing and Terms

Based on the risk assessment, the underwriter determines the appropriate premium, coverage limits, and policy terms. This is the core of ensuring the insurance company is adequately compensated for the risk it’s taking on.

3.5. Approval and Policy Issuance

In some cases, the underwriter may need to obtain approval from senior underwriters or managers before issuing a policy. Once approved, the policy is issued to the client.

4. Factors Considered During Underwriting

Underwriters consider many factors when assessing risk. These factors vary depending on the type of insurance but generally include:

4.1. Applicant History

Past claims, credit history, and other relevant experiences are carefully reviewed. A history of frequent claims or financial instability can increase the perceived risk.

4.2. Current Circumstances

The applicant’s current situation, such as their health, financial status, and occupation, is also considered. These factors can provide insights into the likelihood of future claims.

4.3. Potential Future Risks

Underwriters also assess potential future risks based on industry trends, environmental factors, and other relevant data. This helps them anticipate potential claims and price policies accordingly.

5. Types of Insurance Underwriting

Underwriting processes vary based on the type of insurance:

5.1. Life Insurance Underwriting

Life insurance underwriters assess the risk of insuring an individual’s life. They consider factors such as age, health, lifestyle, and family medical history.

5.2. Health Insurance Underwriting

Health insurance underwriters evaluate the risk of providing health coverage to an individual or group. They consider factors such as medical history, current health status, and lifestyle.

5.3. Property and Casualty Underwriting

Property and casualty underwriters assess the risk of insuring property against damage or loss. They consider factors such as location, construction materials, and security measures.

5.4. Commercial Insurance Underwriting

Commercial insurance underwriters evaluate the risk of insuring businesses. They consider factors such as industry, financial stability, and risk management practices.

6. The Role of Technology in Underwriting

Technology plays an increasing role in modern underwriting. Data analytics and artificial intelligence are used to automate tasks, improve accuracy, and enhance efficiency.

6.1. Data Analytics

Data analytics helps underwriters identify patterns and trends that can inform risk assessment. This can lead to more accurate pricing and better risk management.

6.2. Artificial Intelligence

AI can automate many of the routine tasks involved in underwriting, freeing up underwriters to focus on more complex cases. AI can also improve the accuracy of risk assessments by analyzing large volumes of data.

7. Key Skills for Insurance Underwriters

Successful insurance underwriters possess a unique blend of skills:

7.1. Analytical Skills

Underwriters must be able to analyze complex data and make informed decisions based on their findings.

7.2. Communication Skills

Underwriters need to communicate effectively with applicants, brokers, and other stakeholders.

7.3. Decision-Making Skills

Underwriters must be able to make sound judgments about risk and pricing.

7.4. Industry Knowledge

A strong understanding of the insurance industry and specific lines of coverage is essential.

8. Common Underwriting Challenges and How to Overcome Them

Underwriters face several common challenges:

8.1. Incomplete Information

Applicants may not always provide complete or accurate information. Underwriters must be able to identify missing information and request it from the applicant.

8.2. Evolving Risks

The risk landscape is constantly changing. Underwriters must stay up-to-date on emerging risks and adjust their assessment methods accordingly.

8.3. Competitive Pressure

Underwriters must balance the need to accurately price risk with the pressure to remain competitive in the marketplace.

9. The Impact of Underwriting on Insurance Premiums

Underwriting directly impacts the premiums that policyholders pay. The higher the perceived risk, the higher the premium. Conversely, lower risk typically results in lower premiums.

10. How to Improve Your Chances of Underwriting Approval

Applicants can take steps to improve their chances of underwriting approval:

10.1. Provide Complete and Accurate Information

Ensure your application is complete and accurate. Omissions or inaccuracies can raise red flags and lead to denial.

10.2. Address Potential Concerns

Be prepared to address any potential concerns the underwriter may have. Provide explanations and documentation to support your application.

10.3. Maintain a Good History

A clean claims history and good credit can significantly improve your chances of approval.

11. Underwriting Compliance and Regulations

Insurance underwriting is subject to various regulations and compliance requirements. These regulations aim to protect consumers and ensure fair and equitable treatment.

11.1. State Regulations

Each state has its own set of regulations governing insurance underwriting. Underwriters must be familiar with the regulations in the states where they operate.

11.2. Federal Regulations

Federal regulations, such as the Affordable Care Act, also impact insurance underwriting.

11.3. Compliance Programs

Insurance companies typically have compliance programs in place to ensure adherence to all applicable regulations.

12. The Future of Insurance Underwriting

The future of insurance underwriting is likely to be shaped by technology and data:

12.1. Increased Automation

Automation will continue to streamline the underwriting process, making it faster and more efficient.

12.2. Enhanced Data Analytics

Advanced data analytics will provide underwriters with more insights into risk, leading to more accurate pricing.

12.3. Personalized Insurance Products

Underwriting will play a key role in the development of personalized insurance products tailored to individual needs and risk profiles.

13. Underwriting and Risk Management

Underwriting is a critical component of an insurance company’s overall risk management strategy. By accurately assessing and pricing risk, underwriters help the company manage its exposure and maintain financial stability.

14. The Ethical Considerations in Underwriting

Ethical considerations are paramount in insurance underwriting. Underwriters must ensure they are treating all applicants fairly and equitably, regardless of their background or circumstances.

14.1. Non-Discrimination

Underwriters must not discriminate against applicants based on protected characteristics such as race, gender, or religion.

14.2. Transparency

Underwriters should be transparent with applicants about the factors that influence their underwriting decisions.

14.3. Confidentiality

Underwriters must maintain the confidentiality of applicant information.

15. How Underwriting Differs from Claims Adjusting

While both underwriting and claims adjusting are important functions within an insurance company, they serve different purposes. Underwriting focuses on assessing risk and pricing policies, while claims adjusting involves investigating and settling claims.

16. The Role of Actuaries in Underwriting

Actuaries play a key role in supporting the underwriting process. They use statistical models and data analysis to assess risk and determine appropriate pricing.

17. Understanding Loss Ratios and Their Impact on Underwriting

The loss ratio, which is the ratio of claims paid to premiums earned, is a key metric used to evaluate the performance of an underwriting department. A high loss ratio indicates that the company is paying out more in claims than it is collecting in premiums, which can lead to financial instability.

18. Underwriting Audits: Ensuring Quality and Compliance

Underwriting audits are conducted to ensure that underwriters are adhering to company policies and procedures, as well as all applicable regulations. These audits help identify areas for improvement and ensure the quality of the underwriting process.

19. The Relationship Between Underwriting and Reinsurance

Reinsurance is insurance for insurance companies. It allows insurers to transfer some of their risk to another company. Underwriting plays a key role in determining the amount of reinsurance a company needs to purchase.

20. Career Paths in Insurance Underwriting

Insurance underwriting offers a variety of career paths:

20.1. Entry-Level Underwriter

Entry-level underwriters typically work under the supervision of experienced underwriters, learning the basics of risk assessment and pricing.

20.2. Senior Underwriter

Senior underwriters handle more complex cases and may also have supervisory responsibilities.

20.3. Underwriting Manager

Underwriting managers oversee the underwriting department and are responsible for setting policies and procedures.

20.4. Chief Underwriting Officer

The chief underwriting officer is responsible for the overall underwriting strategy of the insurance company.

21. The Importance of Continuing Education for Underwriters

The insurance industry is constantly evolving, so it’s important for underwriters to stay up-to-date on the latest trends and best practices. Continuing education courses and professional certifications can help underwriters enhance their skills and knowledge.

22. Underwriting in Different Insurance Markets

Underwriting practices can vary depending on the specific insurance market. For example, underwriting in the surplus lines market, which handles high-risk or specialized insurance needs, may be more flexible than underwriting in the standard market.

23. How Economic Conditions Impact Underwriting Decisions

Economic conditions can have a significant impact on underwriting decisions. During economic downturns, underwriters may become more cautious and tighten their underwriting standards.

24. The Underwriting Process for Small Businesses vs. Large Corporations

The underwriting process can differ for small businesses and large corporations. Small businesses may face a simpler underwriting process, while large corporations may require more extensive review and analysis.

25. Common Mistakes to Avoid in the Insurance Application Process

Applicants can avoid common mistakes in the insurance application process by:

25.1. Reading the Application Carefully

Take the time to read the application carefully and understand what information is being requested.

25.2. Providing Accurate Information

Ensure all information provided is accurate and up-to-date.

25.3. Seeking Assistance When Needed

Don’t hesitate to seek assistance from an insurance broker or agent if you have questions or need help completing the application.

26. Underwriting and Customer Service: Balancing Risk and Relationships

Underwriters must balance the need to accurately assess risk with the importance of providing good customer service. Building strong relationships with brokers and applicants can help ensure a smooth and efficient underwriting process.

27. The Impact of Climate Change on Insurance Underwriting

Climate change is having a growing impact on insurance underwriting. Increased frequency and severity of natural disasters are forcing underwriters to reassess their risk models and adjust pricing accordingly.

28. Underwriting and Fraud Prevention

Underwriting plays a critical role in fraud prevention. By carefully reviewing applications and verifying information, underwriters can help detect and prevent fraudulent claims.

29. The Use of Credit Scores in Insurance Underwriting

In some types of insurance, such as auto and homeowners insurance, credit scores may be used as a factor in underwriting. However, the use of credit scores in insurance underwriting is controversial, and some states have restrictions on their use.

30. How to Appeal an Underwriting Decision

If your insurance application is denied or you receive unfavorable terms, you may have the right to appeal the underwriting decision. Contact the insurance company to learn about their appeals process.

31. Underwriting and Policy Renewals

Underwriting is not just for new policies. It also plays a role in policy renewals. At renewal time, underwriters may reassess the risk and adjust the premium or terms accordingly.

32. The Role of Inspections in the Underwriting Process

Inspections are often used in the underwriting process, particularly for property insurance. Inspections can help underwriters assess the condition of the property and identify potential hazards.

33. Underwriting and Policy Exclusions

Policy exclusions are specific risks or perils that are not covered by the insurance policy. Underwriters carefully review policy exclusions to ensure they are appropriate for the risk being insured.

34. The Importance of Documentation in Underwriting

Proper documentation is essential in underwriting. Underwriters must maintain detailed records of all information reviewed and decisions made.

35. Underwriting and Subrogation

Subrogation is the process by which an insurance company recovers payments it has made on a claim from a third party who was responsible for the loss. Underwriting can play a role in identifying potential subrogation opportunities.

36. How to Choose the Right Insurance Coverage for Your Needs

Choosing the right insurance coverage can be complex. Consider your individual needs and circumstances and seek advice from an insurance professional.

36.1. Assess Your Risks

Identify the potential risks you face and determine how much coverage you need to protect yourself.

36.2. Compare Quotes

Get quotes from multiple insurance companies and compare coverage options and prices.

36.3. Read the Policy Carefully

Before purchasing a policy, read it carefully and understand the terms and conditions.

37. Underwriting and the Affordable Care Act (ACA)

The Affordable Care Act (ACA) has significantly impacted health insurance underwriting. The ACA prohibits insurers from denying coverage or charging higher premiums based on pre-existing conditions.

38. Frequently Asked Questions About Insurance Underwriting

Let’s address some common questions about insurance underwriting:

| Question | Answer |

|---|---|

| What is the main goal of underwriting? | The primary goal is to assess risk accurately and price policies appropriately to ensure the insurance company remains financially stable. |

| How does underwriting affect policyholders? | Underwriting directly impacts the premiums policyholders pay. Higher risk leads to higher premiums, while lower risk can result in lower premiums. |

| What factors do underwriters consider? | Factors vary by insurance type but include applicant history, current circumstances, and potential future risks. |

| How has technology changed underwriting? | Technology, such as data analytics and AI, has automated tasks, improved accuracy, and enhanced efficiency in the underwriting process. |

| What is a loss ratio? | The loss ratio is the ratio of claims paid to premiums earned, a key metric for evaluating underwriting performance. |

| Can an underwriting decision be appealed? | Yes, if your insurance application is denied or you receive unfavorable terms, you typically have the right to appeal the underwriting decision. |

| How does climate change affect underwriting? | Climate change is forcing underwriters to reassess risk models and adjust pricing due to the increased frequency and severity of natural disasters. |

| What is the role of actuaries in underwriting? | Actuaries use statistical models and data analysis to assess risk and determine appropriate pricing, supporting the underwriting process. |

| What is subrogation in insurance? | Subrogation is the process by which an insurance company recovers payments made on a claim from a responsible third party. Underwriting can identify opportunities. |

39. Need More Answers? Ask WHAT.EDU.VN!

Still have questions about insurance underwriting or any other topic? Don’t hesitate to ask on WHAT.EDU.VN. Our community of experts is ready to provide you with fast, accurate, and free answers.

Are you struggling to find quick, reliable answers to your questions? Do you feel lost in a sea of information? At WHAT.EDU.VN, we understand your challenges and are here to help. Our platform offers a free service where you can ask any question and receive prompt responses from knowledgeable individuals.

Stop wasting time searching endlessly for answers. Visit WHAT.EDU.VN today and experience the ease and convenience of getting your questions answered for free. Join our community and discover a world of knowledge at your fingertips.

Address: 888 Question City Plaza, Seattle, WA 98101, United States

Whatsapp: +1 (206) 555-7890

Website: WHAT.EDU.VN

Let what.edu.vn be your go-to resource for all your questions. We’re here to provide the answers you need, when you need them, absolutely free. Ask away.